|

BAC511C-BUSINESS ACCOUNTING 1A-1ST OPP- NOV 2025 |

|

|

1 Page 1 |

▲back to top |

nAmlBIA

Un IVE RS ITY

OF SCIEnCE An □

n TECH □ LOGY

HP-GSBq

HAROLD PUPKEWITZ

Gradu ate School of Business

FACULTY OF COMMERCE, HUMAN SCIENCES AND EDUCATION

HAROLD PUPl<EWITZ GRADUATE SCHOOL OF BUSINESS

QUALIFICATION: DIPLOMA IN BUSINESS PROCESS MANAGEMENT

QUALIFICATION CODE: 06DBPM LEVEL: 6

COURSE CODE: BACSllC

COURSE NAME: BUSINESS ACCOUNTING lA

SESSION: NOVEMBER 2025

PAPER: THEORY AND CALCULATIONS (PAPER 1)

DURATION: 3 HOURS

IVIARKS: 100

EXAMINER

FIRST OPPORTUNITY EXAMINATION QUESTION PAPER

Gerhardt Sheehama

MODERATOR Lamed< Odada

--

INSTRUCTIONS

1. This question paper comprises five (5) questions.

2. Answer ALL the questions in blue or black ink only. NO pencil

3. Start each question on a new page in your answer booklet and show all workings.

4. Round off only final answers to two (2) decimal places unless otherwise stated.

5. Questions relating to this examination may be raised in the initial 30 minutes after the

start of the paper. Thereafter, candidates must use their initiative to deal with any

perceived error or ambiguities & any assumption made by the candidate should be

clearly stated .

PERMISSIBLE MATERIALS

Silent, non-programmable calculators

THIS QUESTION PAPER CONSISTS OF 6 PAGES (including this front page)

|

|

2 Page 2 |

▲back to top |

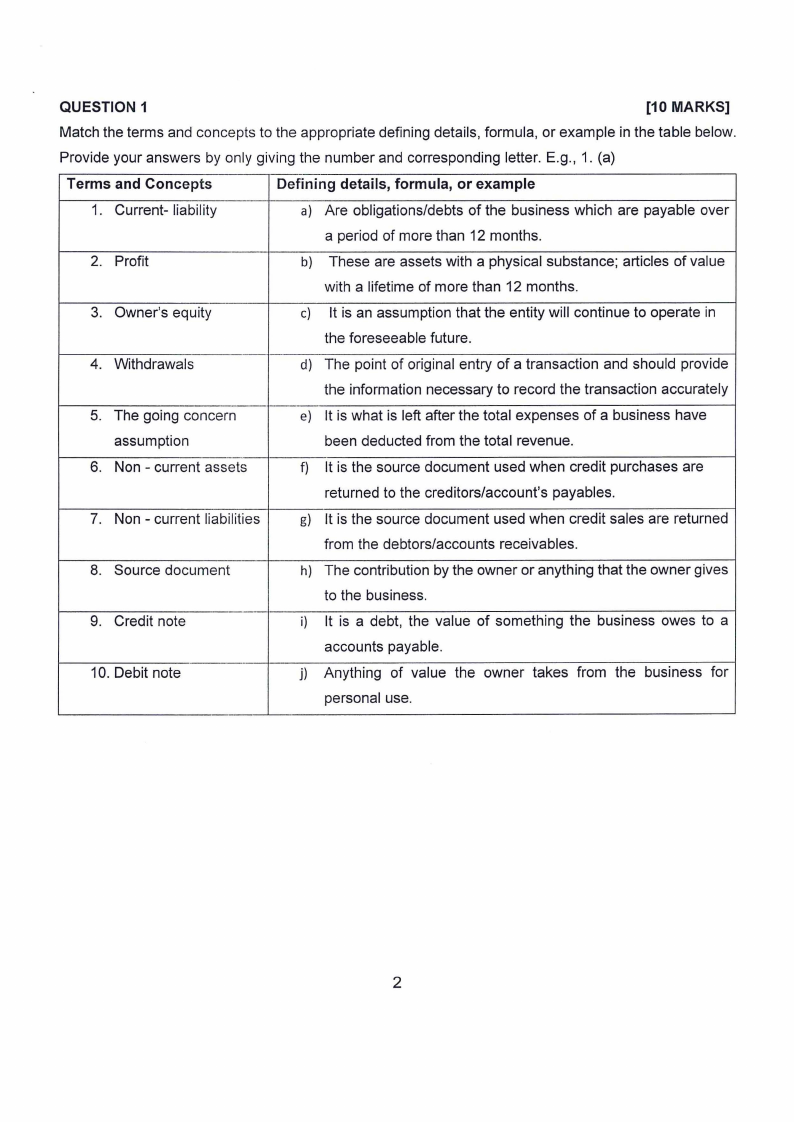

QUESTION 1

[10 MARKS]

Match the terms and concepts to the appropriate defining details, formula, or example in the table below.

Provide your answers by only giving the number and corresponding letter. E.g., 1. (a)

Terms and Concepts

Defining details, formula, or example

1. Current- liability

a) Are obligations/debts of the business which are payable over

a period of more than 12 months.

2. Profit

b) These are assets with a physical substance; articles of value

with a lifetime of more than 12 months.

3. Owner's equity

c) It is an assumption that the entity will continue to operate in

the foreseeable future.

4. Withdrawals

d) The point of original entry of a transaction and should provide

the information necessary to record the transaction accurately

5. The going concern

e) It is what is left after the total expenses of a business have

assumption

been deducted from the total revenue.

6. Non - current assets

f) It is the source document used when credit purchases are

returned to the creditors/account's payables.

7. Non - current liabilities

g) It is the source document used when credit sales are returned

from the debtors/accounts receivables.

8. Source document

h) The contribution by the owner or anything that the owner gives

to the business.

9. Credit note

i) It is a debt, the value of something the business owes to a

accounts payable.

10. Debit note

j) Anything of value the owner takes from the business for

personal use.

2

|

|

3 Page 3 |

▲back to top |

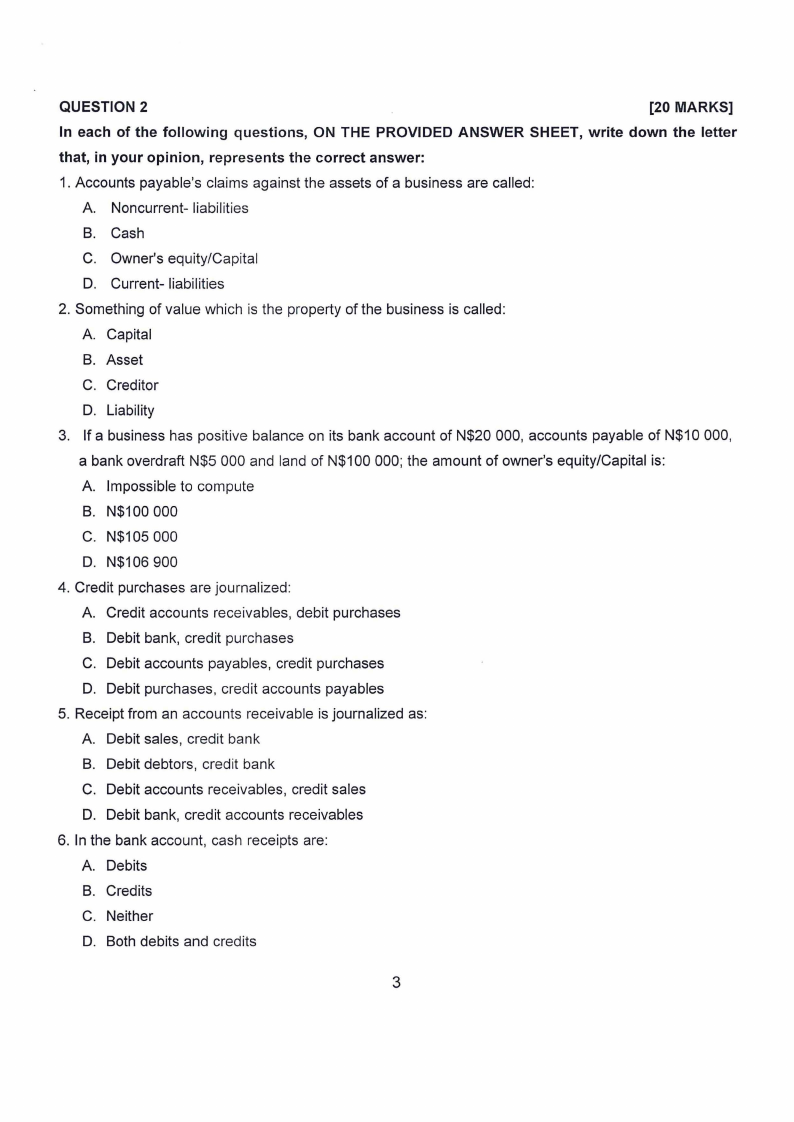

QUESTION 2

[20 MARKS]

In each of the following questions, ON THE PROVIDED ANSWER SHEET, write down the letter

that, in your opinion, represents the correct answer:

1. Accounts payable's claims against the assets of a business are called :

A. Noncurrent- liabilities

B. Cash

C. Owner's equity/Capital

D. Current- liabilities

2. Something of value which is the property of the business is called :

A. Capital

B. Asset

C. Creditor

D. Liability

3. If a business has positive balance on its bank account of N$20 000, accounts payable of N$10 000,

a bank overdraft N$5 000 and land of N$100 000; the amount of owner's equity/Capital is:

A. Impossible to compute

B. N$100 000

C. N$105 000

D. N$106 900

4. Credit purchases are journalized :

A. Credit accounts rece ivables, debit purchases

B. Debit bank, credit purchases

C. Debit accounts payables, credit purchases

D. Debit purchases, credit accounts payables

5. Receipt from an accounts receivable is journalized as:

A. Debit sales, credit bank

B. Debit debtors, credit bank

C. Debit accounts receivables, credit sales

D. Debit bank, credit accounts receivables

6. In the bank account, cash receipts are:

A. Debits

B. Credits

C. Neither

D. Both debits and credits

3

|

|

4 Page 4 |

▲back to top |

7. In the busines bank account, cash payments are:

A. Debits

B. Credits

C. Neither

D. Both debits and credits

8. Nam-Dancer has a dancing school and sells dancing shoes to clients. He won an important

dancing competition. Nam-Dancer proposes to include his dancing skills and experience as

current asset in the statement of financial position. You advised him that this is not allowed.

Which of the following accounting rules apply?

A. The rule periodicity rule

B. The realization rule

C. The quantitative rule

D. The prudence rule

9. A company receives an order in April, posts the goods in May, and receives payment in June.

In this case, under the realization principle, revenue is earned in which month?

A. April

B. May

C. June

D. None

10. Which principle dictates that all data should be captured in such a way that the debit/credit

principle is applied .

A. Matching principle

B. Duality rule

C. Prudence

D. Periodicity principle

[10 x 2 marks = 20 marks]

4

|

|

5 Page 5 |

▲back to top |

QUESTION 3

[10 MARKS]

In each of the following transactions state the error which will not be revealed by a trial balance.

1. A cash receipt of N$5 000 from a trade debtor, Mr. Kaka, has been omitted from the

books

2. Sales to Mr. Lela, N$5 600 was entered in the books as N$6 500

3. Payment of N$1 000 to trade creditor, Mr Xholisa was entered on the debit side of the Cash book

In error and credited to Mr. Xholisa' s ale

4. Billing to Mr. Ben of N$5 000 was wrongly posted to Mr Benry's ale

5. Machinery maintenance of N$1 000 wrongly posted into Machinery ale

[5 x 2 marks = 10 marks]

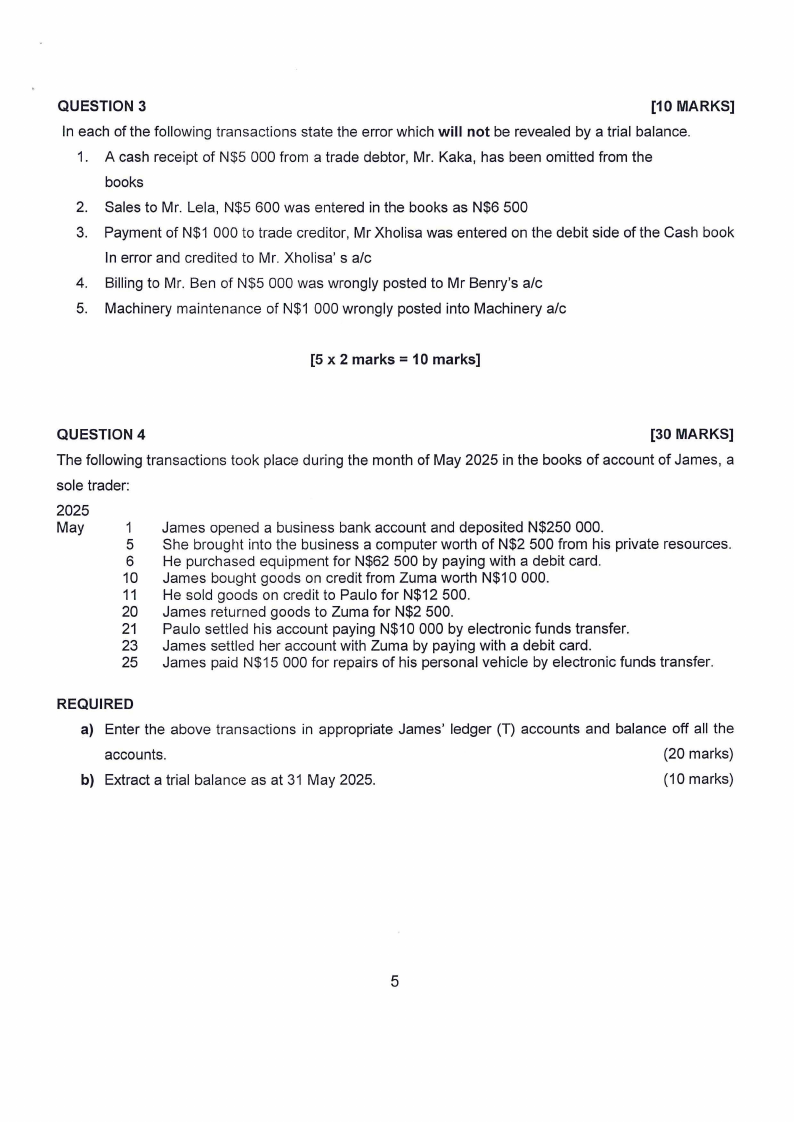

QUESTION 4

[30 MARKS]

The following transactions took place during the month of May 2025 in the books of account of James, a

sole trader:

2025

May

1 James opened a business bank account and deposited N$250 000.

5 She brought into the business a computer worth of N$2 500 from his private resources.

6 He purchased equipment for N$62 500 by paying with a debit card.

10 James bought goods on credit from Zuma worth N$10 000.

11 He sold goods on credit to Paulo for N$12 500.

20 James returned goods to Zuma for N$2 500.

21 Paulo settled his account paying N$10 000 by electronic funds transfer.

23 James settled her account with Zuma by paying with a debit card.

25 James paid N$15 000 for repairs of his personal vehicle by electronic funds transfer.

REQUIRED

a) Enter the above transactions in appropriate James' ledger (T) accounts and balance off all the

accounts.

(20 marks)

b) Extract a trial ba lance as at 31 May 2025.

(10 marks)

5

|

|

6 Page 6 |

▲back to top |

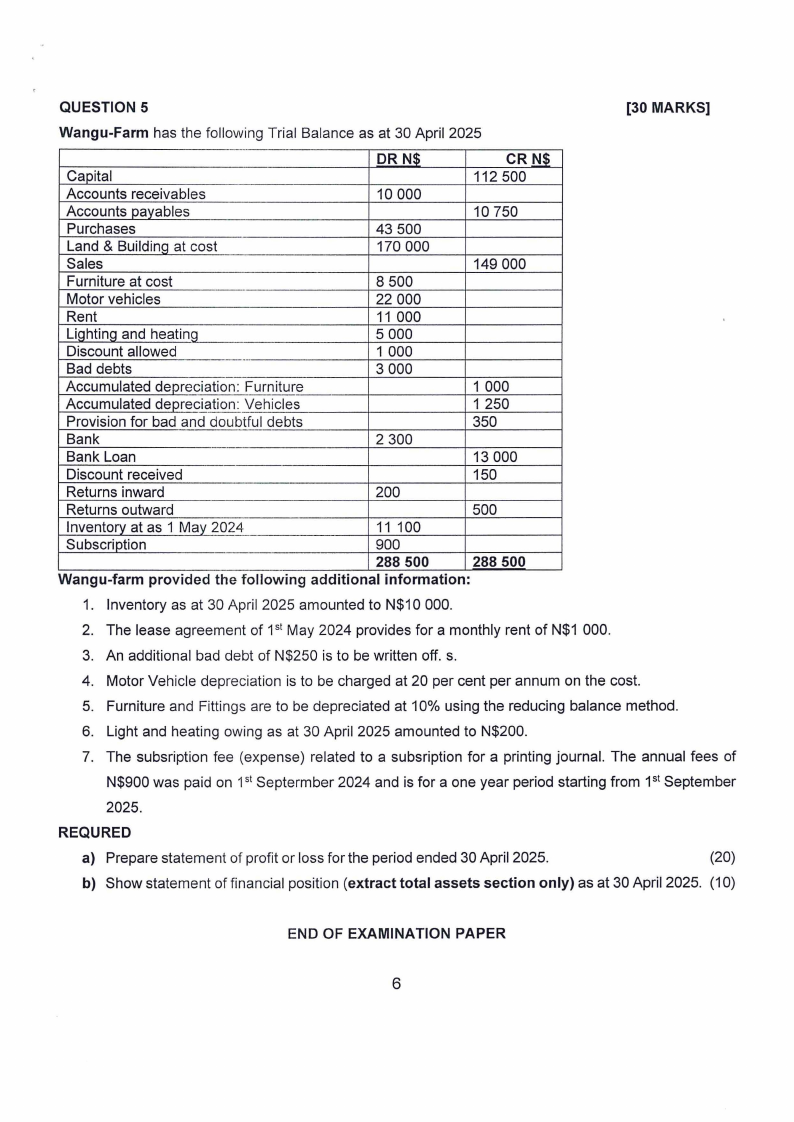

QUESTION 5

[30 MARKS]

Wangu-Farm has the following Trial Balance as at 30 April 2025

DR N$

CRN$

Capital

112 500

Accounts receivables

10 000

Accounts payables

10 750

Purchases

43 500

Land & Building at cost

170 000

Sales

149 000

Furniture at cost

8 500

Motor vehicles

22 000

Rent

11 000

Lighting and heating

5 000

Discount allowed

-

Bad debts

1 000

3 000

Accumulated depreciation: Furniture

1 000

Accumulated depreciation : Vehicles

1 250

Provision for bad and doubtful debts

350

Bank

2 300

Bank Loan

13 000

Discount received

150

Returns inward

200

Returns outward

500

Inventory at as 1 May 2024

11 100

Subscription

900

288 500

288 500

Wangu-farm provided the following additional information:

1. Inventory as at 30 April 2025 amounted to N$10 000.

2. The lease agreement of 1st May 2024 provides for a monthly rent of N$1 000.

3. An additional bad debt of N$250 is to be written off. s.

4. Motor Vehicle depreciation is to be charged at 20 per cent per annum on the cost.

5. Furniture and Fittings are to be depreciated at 10% using the reducing balance method.

6. Light and heating owing as at 30 April 2025 amounted to N$200.

7. The subsription fee (expense) related to a subsription for a printing journal. The annual fees of

N$900 was paid on 1st Septermber 2024 and is for a one year period starting from 1st September

2025.

REQURED

a) Prepare statement of profit or loss for the period ended 30 April 2025.

(20)

b) Show statement of financial position (extract total assets section only) as at 30 April 2025. (10)

END OF EXAMINATION PAPER

6