|

ITA412S-INTRODUCATION TO ACCOUNTING -2ND OPP-DEC 2025 |

|

|

1 Page 1 |

▲back to top |

nAmlBIA UnlVERSITY

OF SCIEnCE An □ TECHn0L0GY

FACULTY OF COMMERCE, HUMAN SCIENCES AND EDUCATION

DEPARTMENT OF ECONOMIC, ACCOUNTING AND FINANCE

QUALIFICATION: BRIDGING PROGRAMME

QUALIFICATION CODE: 04NBR

LEVEL: 4

COURSE CODE: ITA 4125

COURSE NAME: INTRODUCTION TO

ACCOUNTING

SESSION: DECEMBER 2025

DURATION: 3 HOURS

PAPER: THEORY AND CALCULATIONS

MARKS: 100

SECOND OPPORTUNITY EXAMINATION QUESTION PAPER

EXAMINER(S) Dr. D.R. MUZIRA; Ms YANSY CARIDAD ODIO LOPEZ; Mrs LINDSAY JAHS

MODERATOR: Mr. KUHEPA TJONDU

INSTRUCTIONS

1. Answer all questions.

2. Read all the questions carefully before answering.

3. Make sure your name and surname, question number and the

date appears on the answer script.

4. Please ensure that your writing is legible, neat and presentable.

THIS QUESTION PAPER CONSISTS OF 5 PAGES (Including this front page)

|

|

2 Page 2 |

▲back to top |

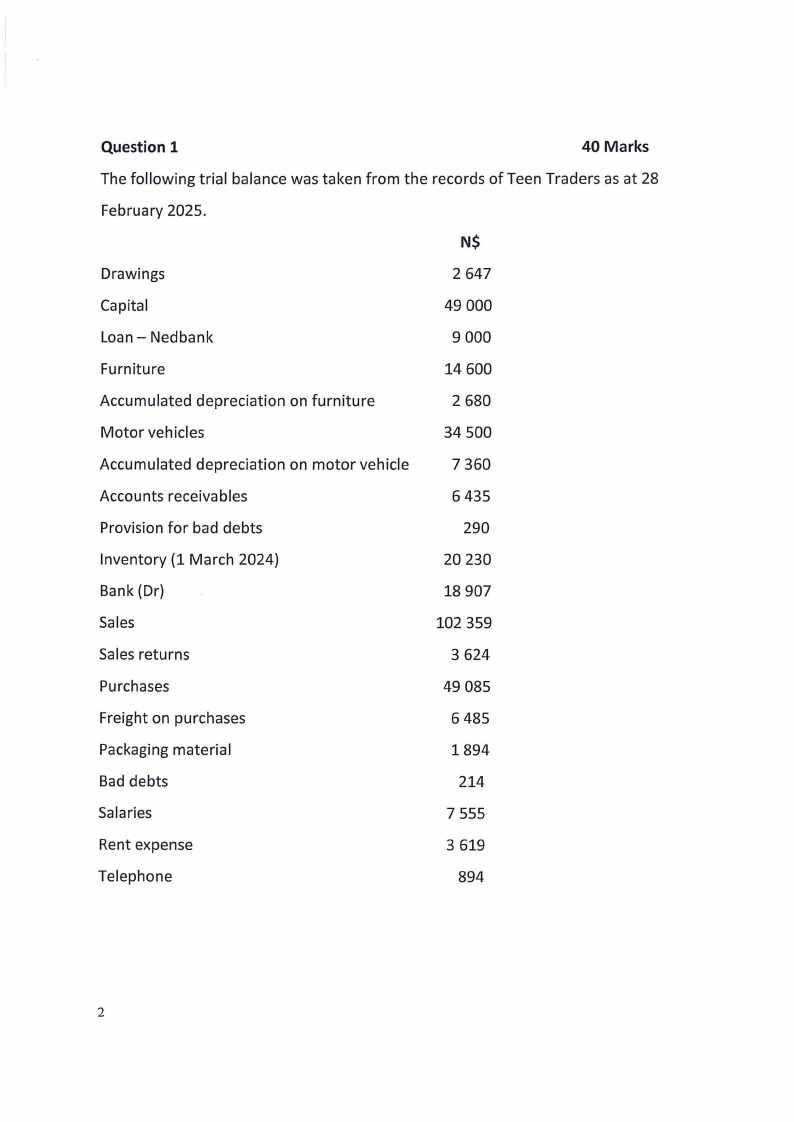

Question 1

40 Marks

The following trial balance was taken from the records of Teen Traders as at 28

February 2025.

N$

Drawings

2 647

Capital

49 000

Loan - Nedbank

9 000

Furniture

14 600

Accumulated depreciation on furniture

2 680

Motor vehicles

34 500

Accumulated depreciation on motor vehicle

7 360

Accounts receivables

6 435

Provision for bad debts

290

Inventory (1 March 2024)

20 230

Bank (Dr)

18 907

Sales

102 359

Sales returns

3 624

Purchases

49 085

Freight on purchases

6 485

Packaging material

1894

Bad debts

214

Salaries

7 555

Rent expense

3 619

Telephone

894

2

|

|

3 Page 3 |

▲back to top |

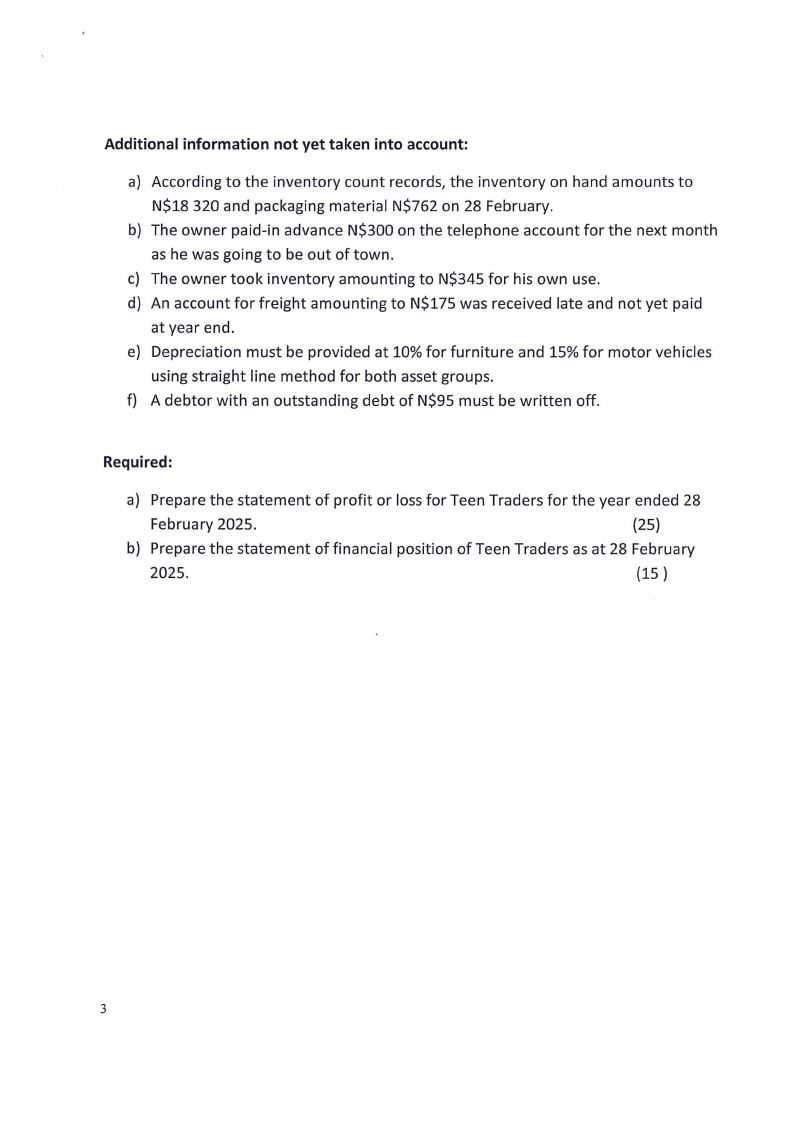

Additional information not yet taken into account:

a) According to the inventory count records, the inventory on hand amounts to

N$18 320 and packaging material N$762 on 28 February.

b) The owner paid-in advance N$300 on the telephone account for the next month

as he was going to be out of town.

c) The owner took inventory amounting to N$345 for his own use.

d) An account for freight amounting to N$175 was received late and not yet paid

at year end.

e) Depreciation must be provided at 10% for furniture and 15% for motor vehicles

using straight line method for both asset groups.

f) A debtor with an outstanding debt of N$95 must be written off.

Required:

a) Prepare the statement of profit or loss for Teen Traders for the year ended 28

February 2025.

(25)

b) Prepare the statement of financial position of Teen Traders as at 28 February

2025.

(15 )

3

|

|

4 Page 4 |

▲back to top |

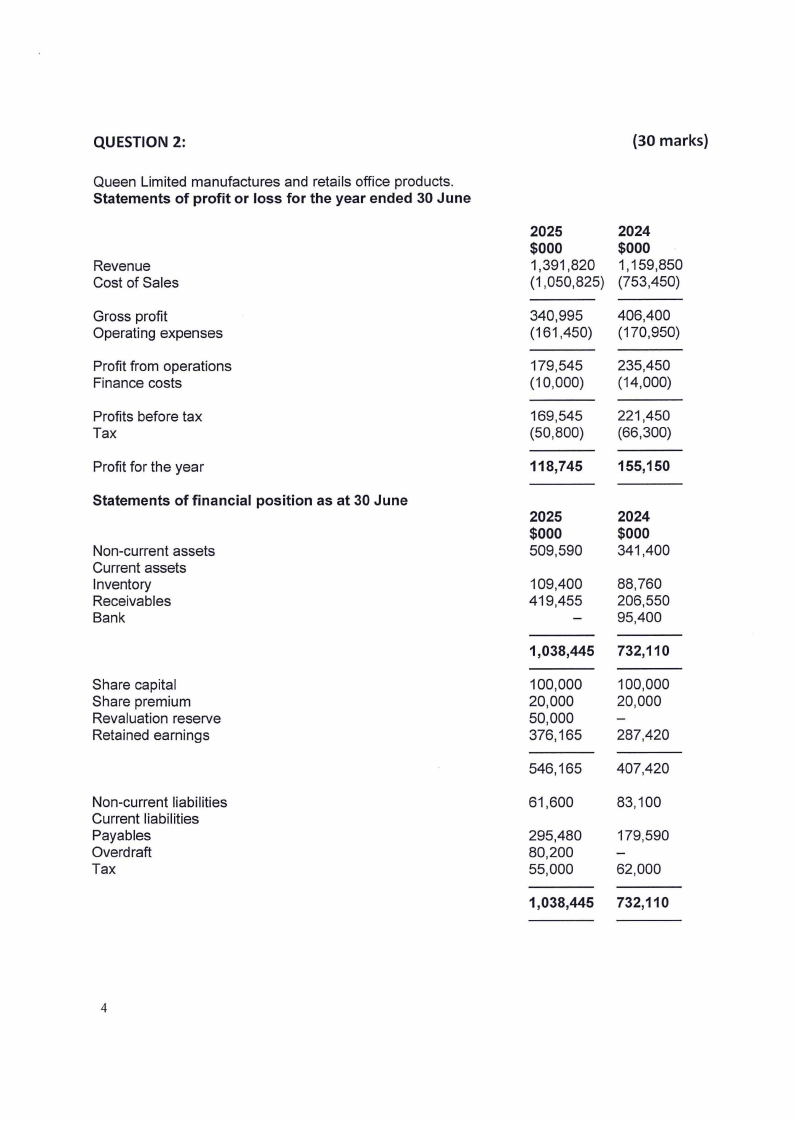

QUESTION 2:

Queen Limited manufactures and retails office products.

Statements of profit or loss for the year ended 30 June

Revenue

Cost of Sales

Gross profit

Operating expenses

Profit from operations

Finance costs

Profits before tax

Tax

Profit for the year

Statements of financial position as at 30 June

Non-current assets

Current assets

Inventory

Receivables

Bank

Share capital

Share premium

Revaluation reserve

Retained earnings

Non-current liabilities

Current liabilities

Payables

Overdraft

Tax

(30 marks)

2025

$000

1,391,820

(1 ,050,825)

2024

$000

1,159,850

(753,450)

340,995 406,400

(161,450) (170,950)

179,545

(10,000)

235,450

(14,000)

169,545

(50,800)

221,450

(66,300)

118,745 155,150

2025

$000

509,590

2024

$000

341,400

109,400

419 ,455

88,760

206,550

95,400

1,038,445 732,110

100,000

20 ,000

50,000

376 ,165

100,000

20,000

287,420

546,165 407,420

61,600

83,100

295,480

80,200

55,000

179,590

62,000

1,038,445 732,110

4

|

|

5 Page 5 |

▲back to top |

Required:

a) Calculate the following ratios for the company for the year ended 30 June 2025:

(20)

i. Gross profit margin

ii. Operating (net) profit margin

iii. Return on capital employed

iv. Inventory days

v. Receivable days

vi. Payable days

vii. Current ratio

viii. Quick ratio

ix. Gearing ratio

x. Interest cover

b) Comment on the performance and position of the company basing on the ratios

calculated above.

(5)

c) State five weaknesses of ratio analysis as a way of evaluating a company's

performance.

(5)

Question 3

30 Marks

a) State the five elements of the financial statement.

(5)

b) Name any five source documents in accounting.

(5)

c) Name five users of accounting information and explain why they are interested

in the information.

(10)

d) State and explain any five errors that can not be revealed by the trial balance

(10)

THE END

5