|

CAH610S-COST AND MANAGEMENT ACCOUNTING FOR HOSPITALITY TOURISM-1ST OPP-NOV 2025 |

|

|

1 Page 1 |

▲back to top |

nAmlBIA UnlVERSITY

OF SCIEnCE Ano TECHnOLOGY

FACULTY OF COMMERCE, HUMAN SCIENCES AND EDUCATION

DEPARTMENT OF HOSPITALITY AND TOURISM

QUALIFICATION: BACHELOR OF CULINARY ARTS & BACHELOR OF TOURISM INNOVATION AND

DEVELOPMENT

QUALIFICATION CODE: 07BCNA & 07BTID LEVEL: 6

COURSE CODE: CAH610S

COURSE NAME: COST & MANAGEMENT

ACCOUNTING FOR HOSPITALITY &

TOURISM

SESSION: NOVEMBER 2025

PAPER: THEORY AND CALCULATIONS (PAPER 1)

DURATION: 3 HOURS

MARKS: 100

EXAMINER

FIRST OPPORTUNITY EXAMINATION QUESTION PAPER

Gerhardt Sheehama

MODERATOR Lamecl< Odada

INSTRUCTIONS

• Answer ALL five (5) questions in blue or black ink only. NO PENCIL.

• Start each question on a new page, number the answers correctly and clearly.

• Write clearly and neatly showing all your workings/assumptions.

• Round off only final answers to two (2) decimal places.

• Questions relating to this examination may be raised in the initial 30 minutes after the start

of the examination. Thereafter, candidates must use their initiative to deal with any

perceived errors or ambiguities and any assumptions made by the candidate should be

clearly stated.

PERMISSIBLE MATERIALS

• Silent, non-programmable calculators

THIS QUESTION PAPER CONSISTS OF _6_ PAGES (including this front page)

|

|

2 Page 2 |

▲back to top |

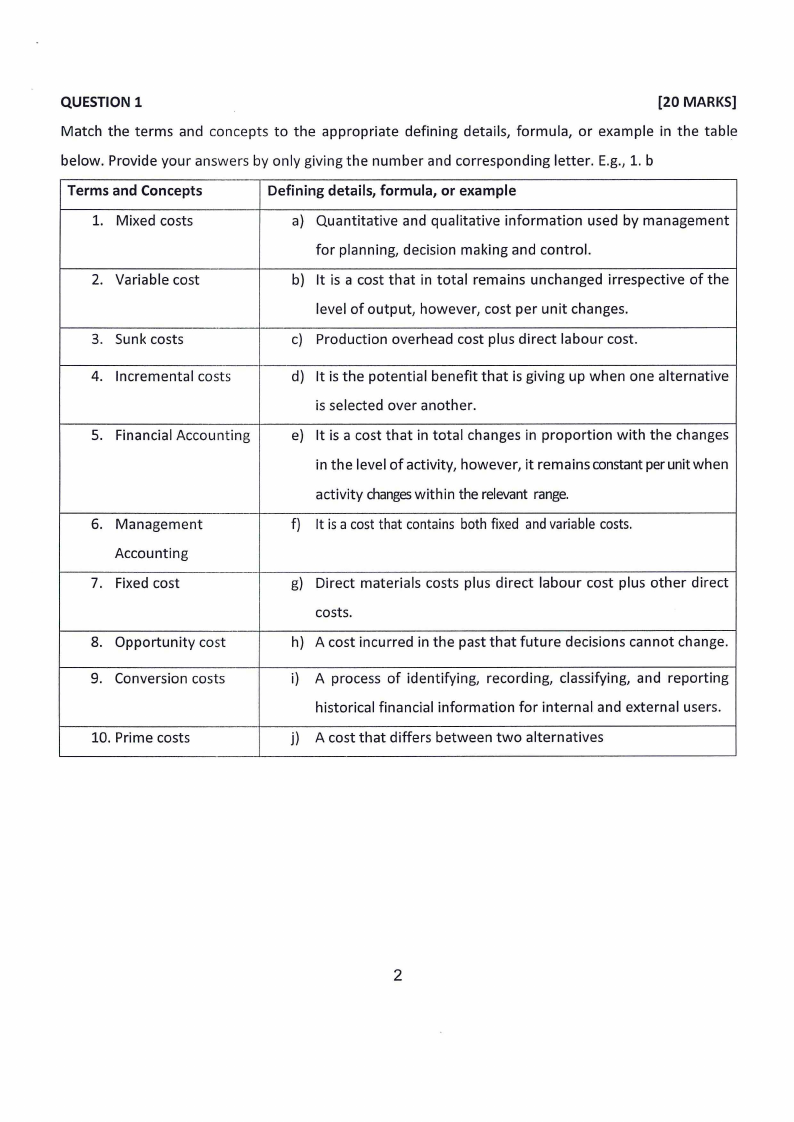

QUESTION 1

[20 MARKS]

Match the terms and concepts to the appropriate defining details, formula, or example in the table

below. Provide your answers by only giving the number and corresponding letter. E.g., 1. b

Terms and Concepts

Defining details, formula, or example

1. Mixed costs

a} Quantitative and qualitative information used by management

for planning, decision making and control.

2. Variable cost

b} It is a cost that in total remains unchanged irrespective of the

level of output, however, cost per unit changes.

3. Sunk costs

c} Production overhead cost plus direct labour cost.

4. Incremental costs

5. Financial Accounting

6. Management

Accounting

7. Fixed cost

8. Opportunity cost

d} It is the potential benefit that is giving up when one alternative

is selected over another.

e} It is a cost that in total changes in proportion with the changes

in the level of activity, however, it remains constant per unit when

activity changes within the relevant range.

f) It is a cost that contains both fixed and variable costs.

g) Direct materials costs plus direct labour cost plus other direct

costs.

h} A cost incurred in the past that future decisions cannot change.

9. Conversion costs

10. Prime costs

i) A process of identifying, recording, classifying, and reporting

historical financial information for internal and external users.

j) A cost that differs between two alternatives

2

|

|

3 Page 3 |

▲back to top |

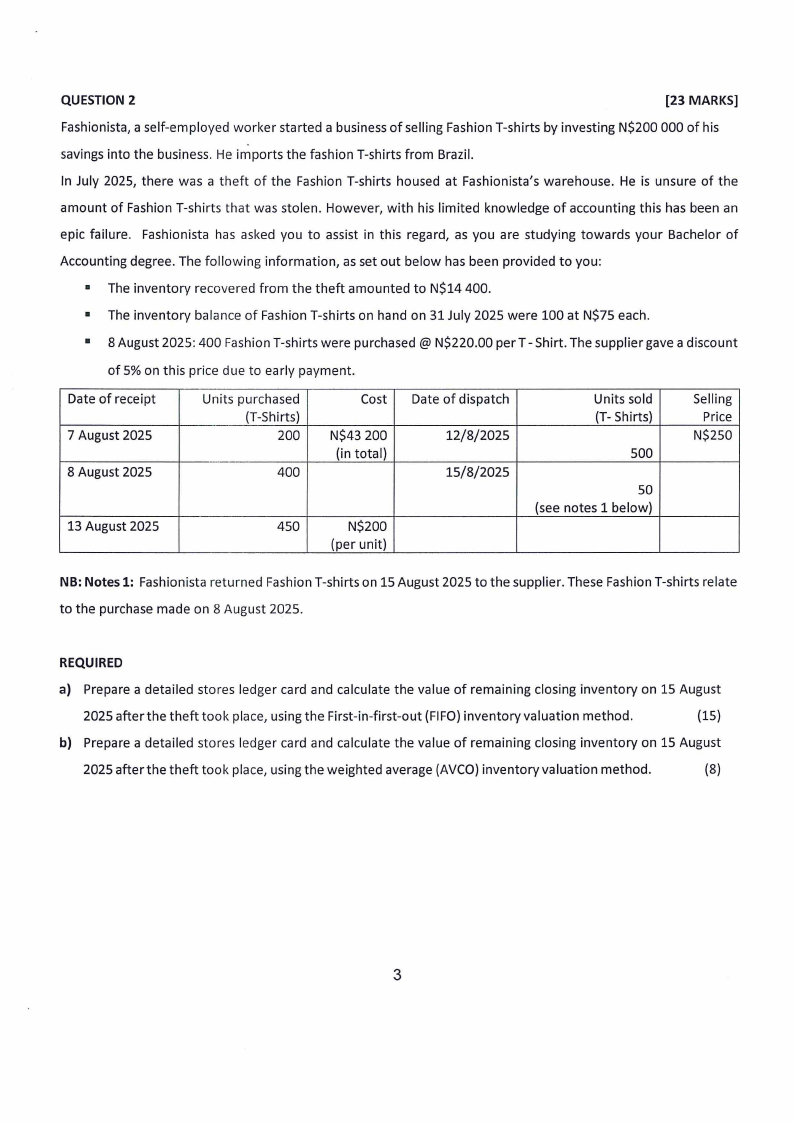

QUESTION 2

[23 MARKS]

Fashionista, a self-employed worker started a business of selling Fashion T-shirts by investing N$200 000 of his

savings into the business . He imports the fashion T-shirts from Brazil.

In July 2025, there was a theft of the Fashion T-shirts housed at Fashionista's warehouse. He is unsure of the

amount of Fashion T-shirts that was stolen . However, with his limited knowledge of accounting this has been an

epic failure . Fashionista has asked you to assist in this regard, as you are studying towards your Bachelor of

Accounting degree. The following information, as set out below has been provided to you:

■ The inventory recovered from the theft amounted to N$14 400.

■ The inventory balance of Fashion T-shirts on hand on 31 July 2025 were 100 at N$75 each.

■ 8 August 2025: 400 Fashion T-shirts were purchased@ N$220.00 per T - Shirt. The supplier gave a discount

of 5% on this price due to early payment.

Date of receipt

7 August 2025

8 August 2025

13 August 2025

Units purchased

(T-Shirts)

200

400

450

Cost

N$43 200

(in total)

N$200

(per unit)

Date of dispatch

12/8/2025

15/8/2025

Units sold

(T- Shirts)

500

so

(see notes 1 below)

Selling

Price

N$250

NB: Notes 1: Fashionista returned Fashion T-shirts on 15 August 2025 to the supplier. These Fashion T-shirts relate

to the purchase made on 8 August 2025.

REQUIRED

a) Prepare a detailed stores ledger card and calculate the value of remaining closing inventory on 15 August

2025 after the theft took place, using the First-in-first-out (FIFO) inventory valuation method.

(15)

b) Prepare a detailed stores ledger card and calculate the value of remaining closing inventory on 15 August

2025 after the theft took place, using the weighted average (AVCO) inventory valuation method.

(8)

3

|

|

4 Page 4 |

▲back to top |

QUESTION 3

(22 MARKS]

Endelela-Twiye Shoe Company operates a chain of shoe stores. The stores sell ten different styles of inexpensive

men's shoes with identical unit costs and selling prices. A unit is defined as one pair of shoes.

Each store has a store manager who is paid a fixed salary. During the current month the stores sold 4 500 pair of

shoes. Endelela-Twiye Shoe Company is trying to determine the desirability of opening another store and provided

the following relevant information:

~

Selling price per pair of shoes

120

Purchase cost per pair of shoes

84

Fixed rent expense per annum

24000

Fixed salary per annum

120 000

REQUIRED

a) Calculate the annual break-even point in units and value (N$).

(6)

b) Calculate the margin of safety in units and value (N$).

(6)

c) Outline five important assumptions underlying the cost-volume-profit analysis.

(10)

QUESTION 4

(15 MARKS]

The transport department of NUST operates a fleet of assorted vehicles. These vehicles are used as the need arises

by the various schools. Each month a statement is prepared for the transport department comparing actual results

with budget.

One of the items in the transport department's monthly statement is the cost of vehicle maintenance. This

maintenance is carried out by the employees of the department. To facilitate his control the transport manager

has asked the future statements should show vehicle maintenance costs analyzed into fixed and variable costs.

Data from the previous six months July to December 2010 inclusive are given below:

Month

July

August

September

October

November

December

Vehicle maintenance costs

N$

12 000

8 250

7 500

9 750

10750

19 500

Vehicle running hours

10500

6 500

4000

7 500

9 000

12 000

4

|

|

5 Page 5 |

▲back to top |

REQUIRED

a) Use the high-low method to determine the total fixed cost and the variable cost per hour.

(4)

b) What vehicle maintenance costs would you expect to be incurred at the level of 11,000 running hours?(S)

c) Determine the fixed cost per hour to be incurred at the level of 3 000 running hours?

(3)

d) Apart from using high-low method to separate the mixed costs, provide examples of other methods. (2)

QUESTION 5

[20 Marks]

a) Explain what you understand by the term "internal rate of return".

(2)

b) Explain two reasons why you would not recommend the payback method as a good technique for the

evaluation of a capital investment.

(4)

c) The management of Wetland Ltd expects a return of at least 14% on all capital investments. The

company presently considering investing in a new machine. Forecasts relating to this machine are as

follows :

Purchase price

Estimated economic life

Annual cash inflows:

End of year 1

2

3

4

N$400 000

3 years

N$150 000

N$225 000

N$180 000

N$100 000

REQUIRED

Make a recommendation to the management of Wetland as to the viability of investing in this new machine.

Use Net Present Value (NPV) method.

(14)

END OF EXAMINATION PAPER

5

|

|

6 Page 6 |

▲back to top |

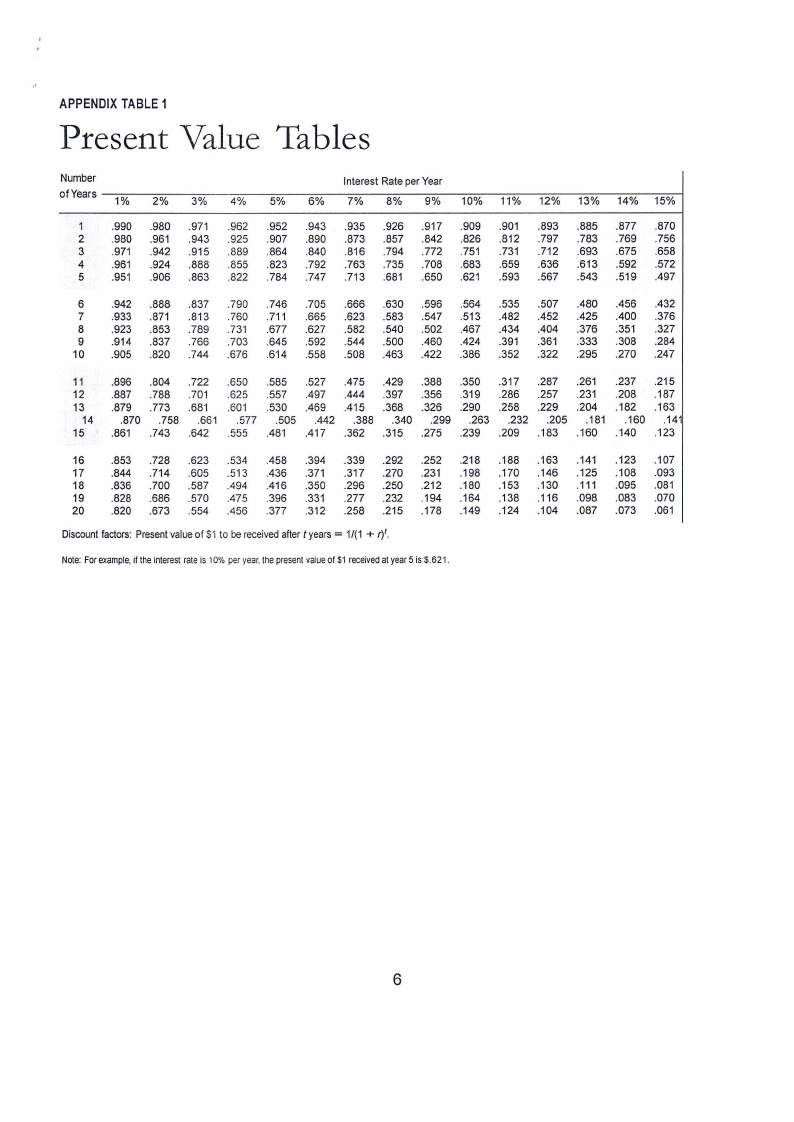

APPENDIX TABLE 1

Present Value Tables

Number

Interest Rate per Year

of Years 1%

2%

3%

4%

5%

6%

7%

8%

9% 10% 11% 12% 13% 14% 15%

1

.990 .980 .971 .962 .952 .943 .935 .926 .917 .909 .901 .893 .885 .877 .870

2

.980 .961 .943 .925 .907 .890 .873 .857 .842 .826 .812 .797 .783 .769 .756

3

.971 .942 .915 .889 .864 .840 .816 .794 .772 .751 .731 .712 .693 .675 .658

4

.961 .924 .888 .855 .823 .792 .763 .735 .708 .683 .659 .636 .613 .592 .572

5

.951 .906 .863 .822 .784 .747 .713 .681 .650 .621 .593 .567 .543 .519 .497

6

.942 .888 .837 .790 .746 .705 .666 .630 .596 .564 .535 .507 .480 .456 .432

7

.933 .871 .813 .760 .711 .665 .623 .583 .547 .513 .482 .452 .425 .400 .376

8

.923 .853 .789 .731 .677 .627 .582 .540 .502 .467 .434 .404 .376 .351 .327

9

.914 .837 .766 .703 .645 .592 .544 .500 .460 .424 .391 .361 .333 .308 .284

10 .905 .820 .744 .676 .614 .558 .508 .463 .422 .386 .352 .322 .295 .270 .247

11

.896 .804 .722 .650 .585 .527 .475 .429 .388 .350 .317 .287 .261 .237 .215

12

.887 .788 .701 .625 .557 .497 .444 .397 .356 .319 .286 .257 .231 .208 .187

13

.879 .773 .681 .601 .530 .469 .415 .368 .326 .290 .258 .229 .204 .182 .163

14

.870 .758 .661 .577 .505 .442 .388 .340 .299 .263 .232 .205 .181 .160 .141

15 .861 .743 .642 .555 .481 .417 .362 .315 .275 .239 .209 .183 .160 .140 .123

16 .853 .728 .623 .534 .458 .394 .339 .292 .252 .218 .188 .163 .141 .123 .107

17 .844 .714 .605 .51 3 .436 .371 .317 .270 .231 .198 .170 .146 .125 .108 .093

18

.836 .700 .587 .494 .416 .350 .296 .250 .212 .180 .153 .130 .111 .095 .081

19

.828 .686 .570 .475 .396 .331 .277 .232 .194 .164 .138 .116 .098 .083 .070

20 .820 .673 .554 .456 .377 .312 .258 .215 .178 .149 .124 .104 .087 .073 .061

Discount factors: Present value of $1 to be received after t years= 1/(1 + r)1.

Note: For example, if the interest rate is 10% per year, the present value of $1 received at year 5 is $. 621 .

6