|

FAC612S-FINANCIAL ACCOUNTING 202-2ND OPP- DEC 2025 |

|

|

1 Page 1 |

▲back to top |

nAmlBIA untVERS:ITY

OF SCIEnCE Ano TECHnOLOGY

FACULTY OF COMMERCE, HUMAN SCIENCES AND EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING AND FINANCE

QUALIFICATION: BACHELOR OF ACCOUNTING

QUALIFICATION CODE: 07BGAC

LEVEL: 6

COURSE CODE: FAC612S

COURSE NAME: FINANCIAL ACCOUNTING 202

DATE: November 2025

DURATION: 3 HOURS

PAPER: THEORY AND CALCULATIONS

MARKS: 100

EXAMINER(S)

SECOND OPPORTUNITY EXAMINATION PAPER

Dr. D. R. Muzira, Ms. A Gustav, Ms. V. Ueitele, Mr. M, Nghiludile and Mr. C.

Mahindi

MODERATOR: Dr. S. Dzomira

INSTRUCTIONS

1. Capture your full name, student number and assessment number on the first page.

2. Answer ALL the questions and manage your time properly.

3. Number each page correctly

4. Write clearly and neatly.

5. Do not write in pencil and do not use tip-ex, as this will not be marked.

6. The names of people and businesses used throughout this assessment do not reflect the

reality and may be purely coincidental.

7. SHOW ALL WORKINGS!

THIS QUESTION PAPER CONSISTS OF 6 PAGES (excluding this front page)

|

|

2 Page 2 |

▲back to top |

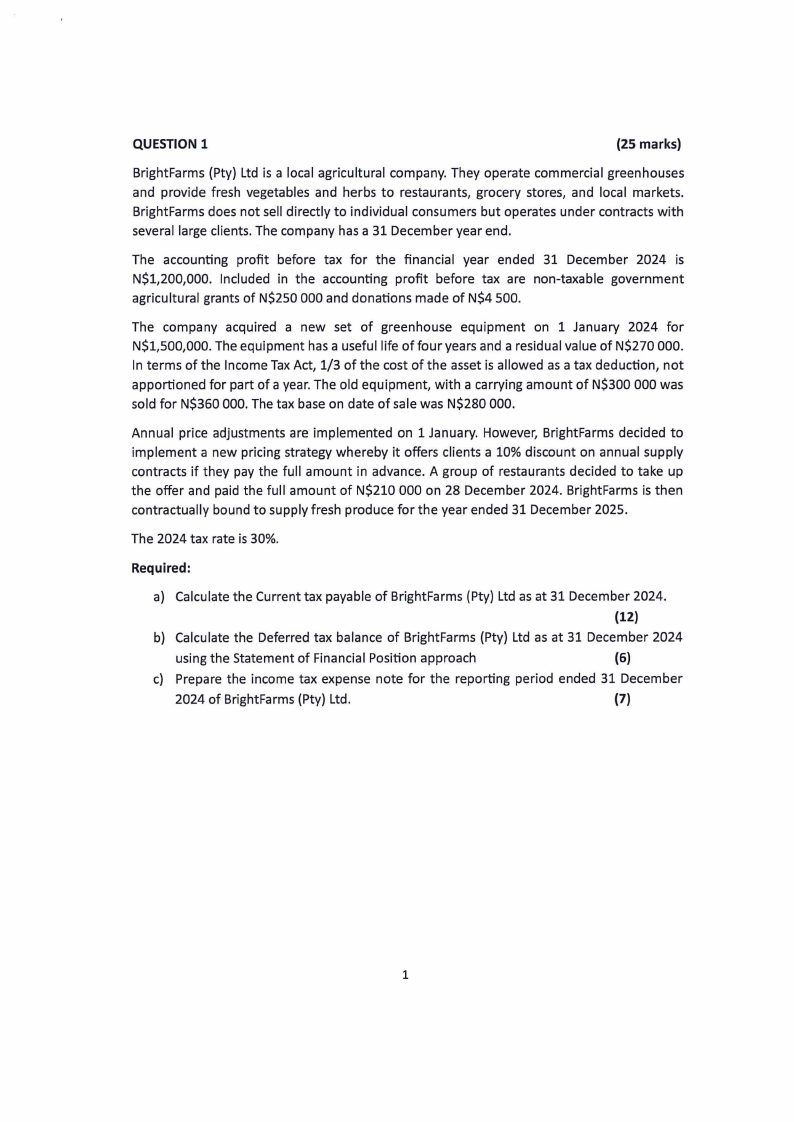

QUESTION 1

(25 marks)

BrightFarms (Pty) Ltd is a local agricultural company. They operate commercial greenhouses

and provide fresh vegetables and herbs to restaurants, grocery stores, and local markets.

BrightFarms does not sell directly to individual consumers but operates under contracts with

several large clients. The company has a 31 December year end.

The accounting profit before tax for the financial year ended 31 December 2024 is

N$1,200,000. Included in the accounting profit before tax are non-taxable government

agricultural grants of N$250 000 and donations made of N$4 500.

The company acquired a new set of greenhouse equipment on 1 January 2024 for

N$1,500,000. The equipment has a useful life of four years and a residual value of N$270 000.

In terms of the Income Tax Act, 1/3 of the cost of the asset is allowed as a tax deduction, not

apportioned for part of a year. The old equipment, with a carrying amount of N$300 000 was

sold for N$360 000. The tax base on date of sale was N$280 000.

Annual price adjustments are implemented on 1 January. However, BrightFarms decided to

implement a new pricing strategy whereby it offers clients a 10% discount on annual supply

contracts if they pay the full amount in advance. A group of restaurants decided to take up

the offer and paid the full amount of N$210 000 on 28 December 2024. BrightFarms is then

contractually bound to supply fresh produce for the year ended 31 December 2025 .

The 2024 tax rate is 30%.

Required:

a) Calculate the Current tax payable of BrightFarms (Pty) Ltd as at 31 December 2024.

(12)

b) Calculate the Deferred tax balance of BrightFarms (Pty) Ltd as at 31 December 2024

using the Statement of Financial Position approach

(6)

c) Prepare the income tax expense note for the reporting period ended 31 December

2024 of BrightFarms (Pty) Ltd.

(7)

1

|

|

3 Page 3 |

▲back to top |

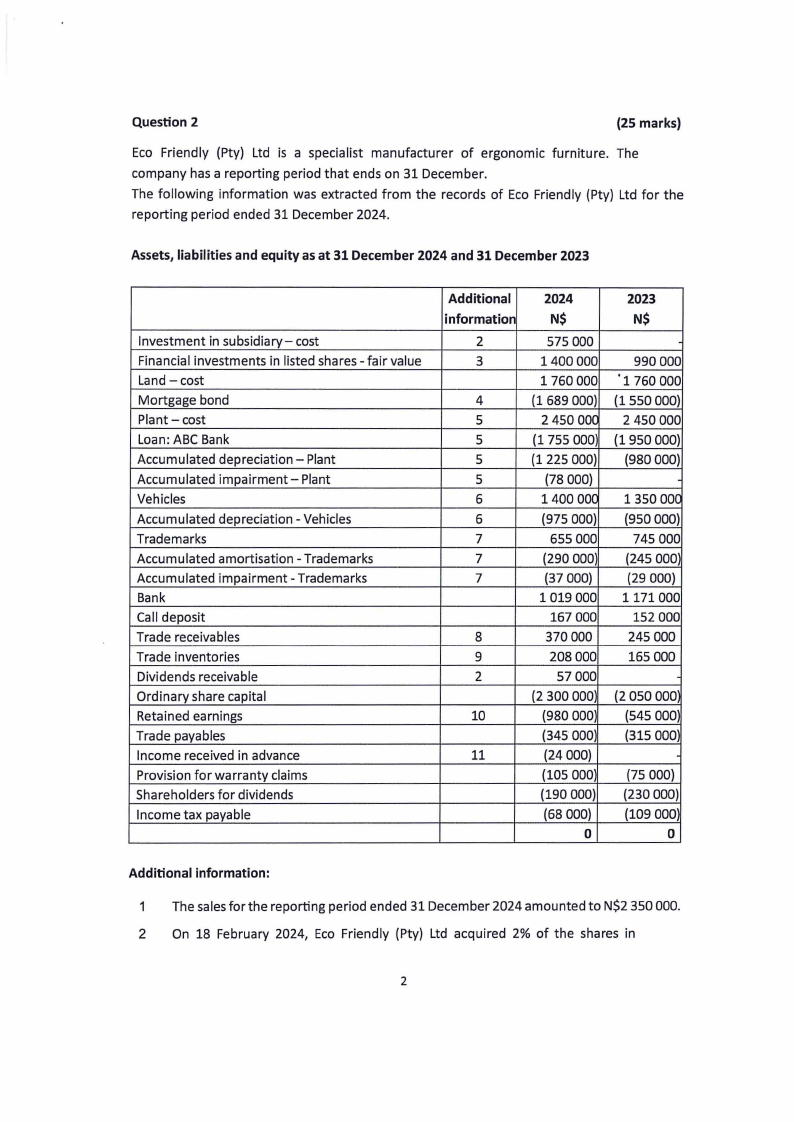

Question 2

(25 marks)

Eco Friendly (Pty) Ltd is a specialist manufacturer of ergonomic furniture. The

company has a reporting period that ends on 31 December.

The following information was extracted from the records of Eco Friendly (Pty) Ltd for the

reporting period ended 31 December 2024.

Assets, liabilities and equity as at 31 December 2024 and 31 December 2023

Investment in subsidiary- cost

Financial investments in listed shares - fair value

Land-cost

Mortgage bond

Plant-cost

Loan: ABC Bank

Accumulated depreciation - Plant

Accumulated impairment- Plant

Vehicles

Accumulated depreciation - Vehicles

Trademarks

Accumulated amortisation - Trademarks

Accumulated impairment - Trademarks

Bank

Call deposit

Trade receivables

Trade inventories

Dividends receivable

Ordinary share capital

Retained earnings

Trade payables

Income received in advance

Provision for warranty claims

Shareholders for dividends

Income tax payable

Additional

information

2

3

4

5

5

5

5

6

6

7

7

7

8

9

2

10

11

2024

N$

575 000

1400 000

1760000

(1689 000)

2 450 ooc

(1 755 000)

(1225 000)

(78 000)

1400 ooc

(975 000)

655 000

(290 000)

(37 000)

1019000

167 000

370 000

208 000

57000

(2 300 000

(980 000

(345000)

(24 000)

(105 000)

(190 000)

(68 000)

0

2023

N$

990 000

•1760000

(1550 000)

2 450 000

(1950 000)

(980 000)

1350 ooc

(950 000)

745 000

(245 000)

(29 000)

1171000

152 000

245 000

165 000

(2 050 000

(545 000

(315 000)

(75 000)

(230 000)

(109 000

0

Additional information:

1 The sales for the reporting period ended 31 December 2024 amounted to N$2 350 000.

2 On 18 February 2024, Eco Friendly (Pty) Ltd acquired 2% of the shares in

2

|

|

4 Page 4 |

▲back to top |

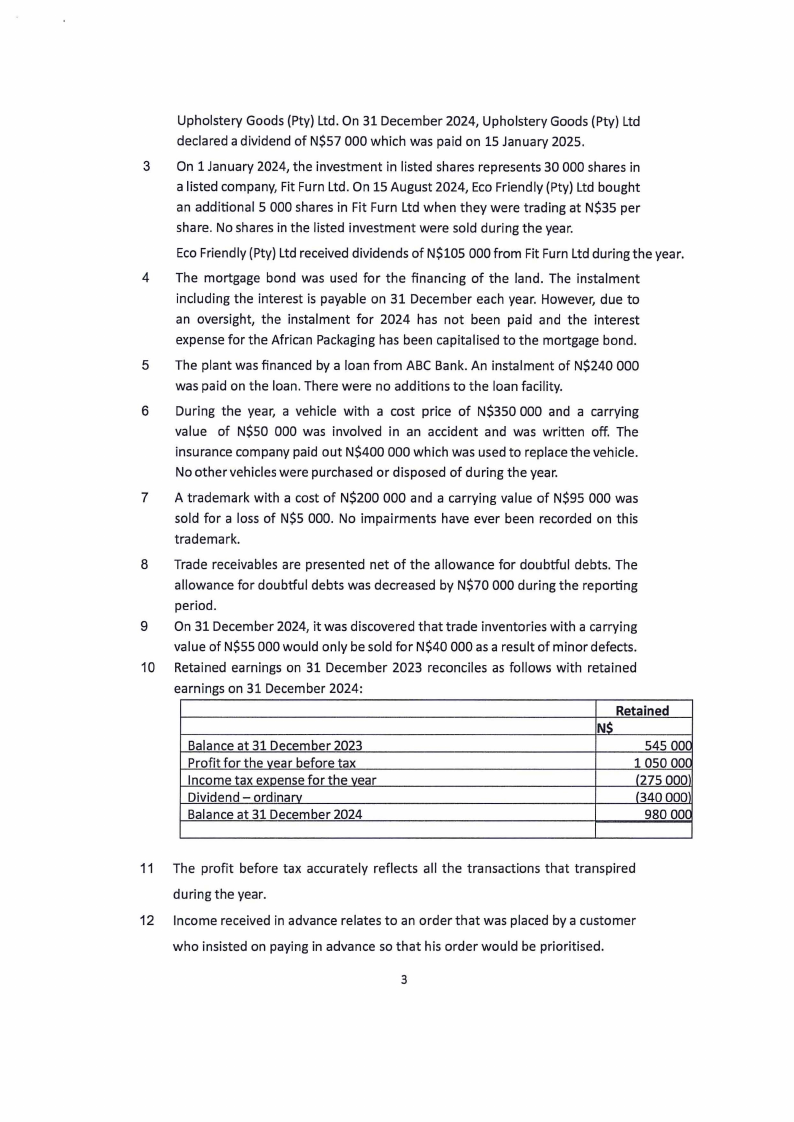

Upholstery Goods (Pty) Ltd. On 31 December 2024, Upholstery Goods (Pty) Ltd

declared a dividend of N$57 000 which was paid on 15 January 2025.

3 On 1 January 2024, the investment in listed shares represents 30 000 shares in

a listed company, Fit Furn Ltd. On 15 August 2024, Eco Friendly (Pty) Ltd bought

an additional 5 000 shares in Fit Furn Ltd when they were trading at N$35 per

share. No shares in the listed investment were sold during the year.

Eco Friendly (Pty) Ltd received dividends of N$105 000 from Fit Furn Ltd during the year.

4 The mortgage bond was used for the financing of the land. The instalment

including the interest is payable on 31 December each year. However, due to

an oversight, the instalment for 2024 has not been paid and the interest

expense for the African Packaging has been capitalised to the mortgage bond.

5 The plant was financed by a loan from ABC Bank. An instalment of N$240 000

was paid on the loan. There were no additions to the loan facility.

6 During the year, a vehicle with a cost price of N$350 000 and a carrying

value of N$50 000 was involved in an accident and was written off. The

insurance company paid out N$400 000 which was used to replace the vehicle.

No other vehicles were purchased or disposed of during the year.

7 A trademark with a cost of N$200 000 and a carrying value of N$95 000 was

sold for a loss of N$5 000. No impairments have ever been recorded on this

trademark.

8 Trade receivables are presented net of the allowance for doubtful debts. The

allowance for doubtful debts was decreased by N$70 000 during the reporting

period.

9 On 31 December 2024, it was discovered that trade inventories with a carrying

value of N$55 000 would only be sold for N$40 000 as a result of minor defects.

10 Retained earnings on 31 December 2023 reconciles as follows with retained

earnings on 31 December 2024:

Balance at 31 December 2023

Profit for the vear before tax

Income tax exoense for the vear

Dividend - ordinarv

Balance at 31 December 2024

Retained

N$

545 DOC

1050 DOC

(275 000

(340 000

980 00(

11 The profit before tax accurately reflects all the transactions that transpired

during the year.

12 Income received in advance relates to an order that was placed by a customer

who insisted on paying in advance so that his order would be prioritised.

3

|

|

5 Page 5 |

▲back to top |

13 The cash payments to suppliers and employees as it appears in the statement

of cashflows has correctly been determined to be N$1 081 000.

Required:

a) Present the statement of cashflows of Eco Friendly (Pty) Ltd for the reporting period

ended 31 December 2024 using the direct method. Show all workings. (25)

Question 3

(25 marks)

This question consists of two unrelated parts:

PART A

(10 marks)

1. On 31 January 2025, the marketing director of Sunrise Airways Ltd informed management

of the possibility that the company's new logo, which appears on all its aircraft, would

have to be changed after complaints had been received from its main competitor, Tropical

Airlines Ltd . The competitor claimed that the new logo was similar to its own logo and

started legal proceedings against Sunrise Airways Ltd . However, on 28 February 2025, the

legal advisors of Sunrise Airways Ltd were of the opinion that it is not probable that

Tropical Airlines Ltd will be successful with their legal claim against the company.

2. After a review of the company's insurance policy covering possible claims from passengers

for damaged or lost baggage and flight delays, the financial director of Sunrise Airways Ltd

recommended that the company cancel their current insurance policy with Quicksure Ltd

on 1 March 2025 and self-insure in future . Based on previous years' records, the financia l

director estimated that these claims from passengers amounted to approximately

N$240,000 a year. For the year ended 28 February 2024, 25 claims amounting to

N$185,000 in total were submitted by passengers. On 27 February 2024, it was probable

that these claims of N$185 000 would be successful. On 15 April 2024, the court ruled that

an amount of N$178 000 should be paid for all the claims submitted during the previous

financial year, which was subsequently paid out. Claims amounting to N$260 000 in total

were submitted by passengers during the year ended 28 February 2025. The final outcome

of these claims will be determined during the court hearings scheduled for April 2025. On

28 February 2025, Sunrise Airways Ltd's legal advisors advised the company that the

possibility is remote that the company will be found liable for N$65 000 of the claims

submitted during the current financial year due to incomplete records.

Required:

i. Prepare the journal entries for the above-mentioned transactions in the books of

Sunrise Airways Ltd for the year ended 28 February 2025.

(6)

4

|

|

6 Page 6 |

▲back to top |

ii. Disclose the Contingent liability in the notes to the annual financial statements of

Sunrise Airways Ltd for the year ended 28 February 2025 according to the

requirements of IAS 37, Provisions, contingent liabilities and contingent assets. (4)

PART B

15 marks

Dripp Limited's had the following as events that occurred or information became available

between 1 July 2025 and 31 August 2025 (the date the financial statements were authorised

for issue): Dripp's reporting period ended 30 June 2025 .

a. A debtor that owed Dripp N$160 000 at year-end had their factory destroyed in a

labour strike in June 2025. As a result, this debtor has filed for insolvency and will

probably pay 40% of the balance owing. Dripp was unaware of this debtor's financial

difficulties on 30 June 2025.

b. Dripp declared a dividend on 20 August 2025 of N$200 000.

c. A debtor that owed Dripp N$10 000 at year-end was in financial difficulties at year-

end and, as a result, Dripp processed an impairment loss adjustment of N$2 000

against this account. In July 2025, the debtor's lawyers announced that it would be

paying 70% of all debts.

d. Inventory carried at N$120 000 at year-end was sold for N$100 000 in July 2025. It had

been damaged in a flood during May 2025.

e. Current tax expense of N$45 000 had been incorrectly debited to rent revenue in June

2025.

Required:

None of the above events has yet been considered. For each event, explain whether the event

is an adjusting or non-adjusting event after the reporting period. If the event is an adjust event,

provide the relevant journal entries.

(15)

5

|

|

7 Page 7 |

▲back to top |

Question 4

(25 marks)

SunnyBird Ltd purchased 100 000 debentures from NestEgg Ltd on 1 January 2025 at their fair

value of N$21,50 per debenture. The debentures were purchased for collecting contractual

cash flows of interest and principal only on specified dates.

The debentures have a face value of N$20 per debenture, and interest is paid annually on 31

December at a coupon interest rate of 12% per annum. The debentures will be redeemed on

31 December 2029 at their face value. SunnyBird Ltd incurred transaction costs of N$25 000

when it purchased the debentures.

The effective interest rate (IRR) of debentures is 9,7089%.

Required:

a. Discuss how the investment in the debentures would be classified and measured in

terms of IFRS 9, in the financial statements of SunnyBird Ltd.

(8)

b. Prepare all the journal entries (except for any impairment journal entries) relating to

the investment in the debentures for the financial year ending 31 December 2025 and

2026. Journal narrations are required. Show all workings.

(17)

END OF EXAMINATION QUESTION PAPER

6