Study Material

Prescribed Textbooks

• W Badenhorst, L, Kotze & D Pretorious, GAAP HANDBOOK, Financial accounting and reporting

practice, Volume 1 and 2, 2022,. LexisNexis

• Descriptive Accounting, 20th edition, LexisNexis (Koppeschaar, Binnekade et al.). Lexis Nexis

Recommended Textbooks

• C. Service, Gripping GAAP, Your guide to International financial reporting standards. Lexis

Nexis

• Stainbank, L., Oakes, D. & Razak, M. A student's guide to international financial reporting (9th

Edition). Eston, KZN. S & 0 Publishing.

• Vorster Q., Koornhof C., Oberholster J., Koppeschaar Z. (Latest). Descriptive Accounting IFRS

focus. LexisNexis, Butterworths

• Pretorius, Venter, Von Well, Wingard. (Latest) GAAP Handbook. LexisNexis, Butterworths

• Elliot B. and Elliot J. (Latest). Financial Accounting and reporting. Harlow Pearson Education Ltd

• The South African Institute of Chartered Accountants. (Latest). International Financial Reporting

Standards (IFRS) volumes 1 & 2. (Latest). LexisNexis, Butterworths.

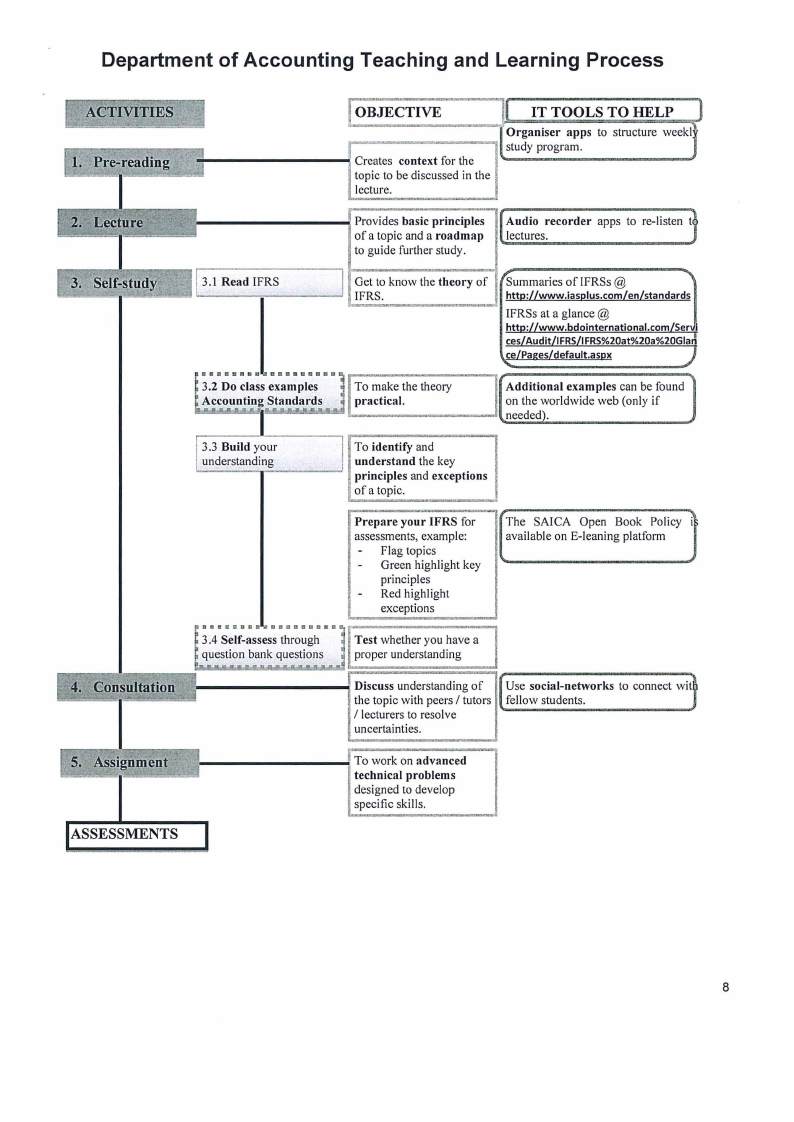

Copies are available in the library. These are excellent resources for the topics that you struggle with as

they work through the standards on a concept by concept basis at a time with examples throughout. They

will require more time to be invested in a topic but will be worth your while. Not recommended for each and

every topic - use it as needed.

Competences and Outcomes

Accounting is a professional course and require certain degree of skills and competencies, therefore, in

order to successfully complete this course, you would need to master four overarching competencies:

Ethical behaviour and professionalism Outcomes:

• A student needs to act competently with honesty and integrity when completing and submitting

assessment tasks.

• A student should perform work competently and with due care.

• A student needs to adhere to the Department of Accounting Code of Ethics

Personal attributes Outcomes:

• A student needs to be able to self-manage his/her learning process to be well-prepared for tests;

completing all assigned work and self-assesses performance.

• A student needs to be able to self-manage his/her stress levels both during the preparation for and

writing of tests.

• A student should treat others in a professional manner, that is you should treat others respectfully,

courteously and equitably.

• A student should strive to be a life-long learner.

• A student needs to be able to manage his/her time effectively both during the preparation for and

writing of tests, including the ability to organise tasks logically.

Professional skills Outcomes:

• A student needs to be able to examine and interpret information and ideas provided in the

background information of case studies in assignments and tests critically.

• A student needs to be able to communicate solutions effectively and efficiently within his/her

assignments and tests.

3