|

ECM712S-ECONOMETRICS-1ST OPP-JUNE 2025 |

|

|

1 Page 1 |

▲back to top |

n Am I BI A u n IVE RS ITV

OF SCIEnCE Ano TECHnOLOGY

FACULTY OF COMMERCE, HUMAN SCIENCESAND EDUCATION

DEPARTMENT OF ECONOMICS,ACCOUNTING AND FINANCE

QUALIFICATION:BACHELOROF ECONOMICS

QUALIFICATIONCODE: 12BECO

LEVEL: 7

COURSECODE: ECM712S

COURSENAME: ECONOMETRICS

SESSION:JUNE 2025

DURATION: 3 HOURS

PAPER:THEORY

MARKS: 100

FIRST OPPORTUNITY EXAMINATION QUESTION PAPER

EXAMINER(S)

MR EDENTATE SHIPANGA

MODERATOR:

MR. GEBHARDLUCKYSHIGWEDHA

INSTRUCTIONS

1. Answer ALL the questions.

2. Write clearly and neatly.

3. Number the answers clearly.

PERMISSIBLE MATERIALS

1. PEN,

2. PENCIL

3. CALCULATOR

THIS QUESTION PAPERCONSISTSOF 4 PAGES{Including this front page)

|

|

2 Page 2 |

▲back to top |

·SECTION A

MULTIPLE CHOICE QUESTIONS

r20 MARKSl

I. The residual from a standard regression model is defined as

a) The difference between the actual value, y, and the mean, y-bar

b) The difference between the fitted value, y-hat, and the mean, y-bar

c) The difference between the actual value, y, and the fitted value, y-hat

d) The square of the difference between the fitted value, y-hat, and the mean, y-bar

2. All of the following are possible effects of multicollinearity EXCEPT:

a) the variances of regression coefficients estimators may be larger than expected

b) the signs of the regression coefficients may be opposite of what is expected

c) a significant F ratio may result even though the t ratios are not significant

d) removal of one data point may cause large changes in the coefficient estimates

e) the VIF is zero

3. In linear regression, the assumption of homoscedasticity is needed for

I.

unbiasedness

11. simple calculation of variance and standard errors of coefficient estimates.

Ill. the claim that the OLS estimator is BLUE.

a) I only.

b) B) II only.

c) C) III only.

d) D) II and III only.

e) E) I, II, and III.

4. The statistical significance of a parameter in a regression model refers to:

a) The conclusion of testing the null hypothesis that the parameter is equal to zero, against the

alternative that it is non-zero.

b) The probability that the OLS estimate of this parameter is equal to zero.

c) The interpretation of the sign (positive or negative) of this parameter.

d) All of the above

5. Which of the following is/are consequences of over specifying a model (including irrelevant variables on

the right-hand-side)?

I. The variance of the estimators may increase.

II. The variance of the estimators may stay the same.

III. Bias of the estimators may increase.

a) I only.

b) II only.

c) III only.

d) I and Il only.

e) I, II, and III.

6. Heteroscedasticity means that

a) Homogeneity cannot be assumed automatically for the model.

b) the observed units have different preferences.

c) the variance of the error term is not constant.

d) agents are not all rational.

7. In a two regressor regression model, if you exclude one of the relevant variables then

a) OLS is no longer unbiased, but still consistent.

b) the OLS estimator no longer exists.

c) you are no longer controlling for the influence of the other variable.

d) it is no longer reasonable to assume that the errors are homoscedastic.

|

|

3 Page 3 |

▲back to top |

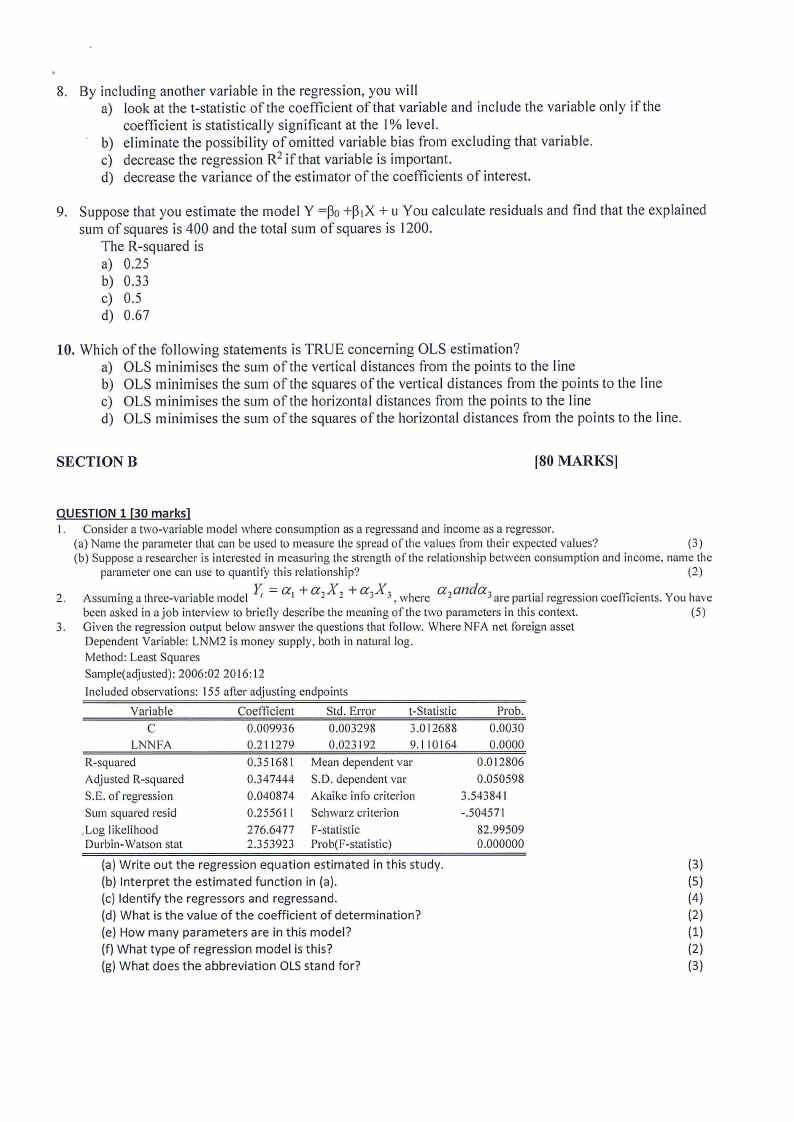

8. By including another variable in the regression, you will

a) look at the t-statistic of the coefficient of that variable and include the variable only if the

coefficient is statistically significant at the l % level.

b) eliminate the possibility of omitted variable bias from excluding that variable.

c) decrease the regression R2 if that variable is important.

d) decrease the variance of the estimator of the coefficients of interest.

9. Suppose that you estimate the model Y =~o +~1X + u You calculate residuals and find that the explained

sum of squares is 400 and the total sum of squares is 1200.

The R-squared is

a) 0.25

b) 0.33

c) 0.5

d) 0.67

10. Which of the following statements is TRUE concerning OLS estimation?

a) OLS minimises the sum of the ve11ical distances from the points to the line

b) OLS minimises the sum of the squares of the vertical distances from the points to the line

c) OLS minimises the sum of the horizontal distances from the points to the line

d) OLS minimises the sum of the squares of the horizontal distances from the points to the line.

SECTIONB

f80 MARKS]

QUESTION 1 (30 marks]

I. Consider a two-variable model where consumption as a regressand and income as a regressor.

(a) Name the parameter that can be used to measure the spread of the values from their expected values?

(3)

(b) Suppose a researcher is interested in measuring the strength of the relationship between consumption and income, name the

parameter one can use to quantity this relationship?

(2)

2.

Assum1•11gat 11ree-vana"bl e 1110delY,=a

1

+a1-X

-1

+a,X,

J

·',

w 11ere

a -1anda,J are parti.a 1regressio. n

coet .t1i.c1ents.You have

been asked in a job interview to briefly describe the meaning of the two parameters in this context.

(5)

3. Given the regression output below answer the questions that follow. Where NFA net foreign asset

Dependent Variable: LNM2 is money supply, both in natural log.

Method: Least Squares

Sarnple(adjusted): 2006:02 2016: 12

Included observations: 155 after adjusting endpoints

Variable

Coefficient

Std. Error

t-Statistic

Prob.

C

LNNFA

R-squared

Adjusted R-squared

S.E. of regression

Sum squared resid

,Log likelihood

Durbin-Watson stat

0.009936

0.211279

0.351681

0.347444

0.040874

0.25561 I

276.6477

2.353923

0.003298

3.012688

0.0030

0.023192

9.110164

0.0000

Mean dependent var

0.0 I2806

S.D. dependent var

0.050598

Akaike info criterion

3.543841

Schwarz criterion

-.504571

F-statistic

Prob(F-statistic)

82.99509

0.000000

(a) Write out the regression equation estimated in this study.

(3)

(b) Interpret the estimated function in (a).

(5)

(c) Identify the regressors and regressand.

(4)

(d) What is the value of the coefficient of determination?

(2)

(e) How many parameters are in this model?

(1)

(f) What type of regression model is this?

(2)

(g) What does the abbreviation OLSstand for?

(3)

|

|

4 Page 4 |

▲back to top |

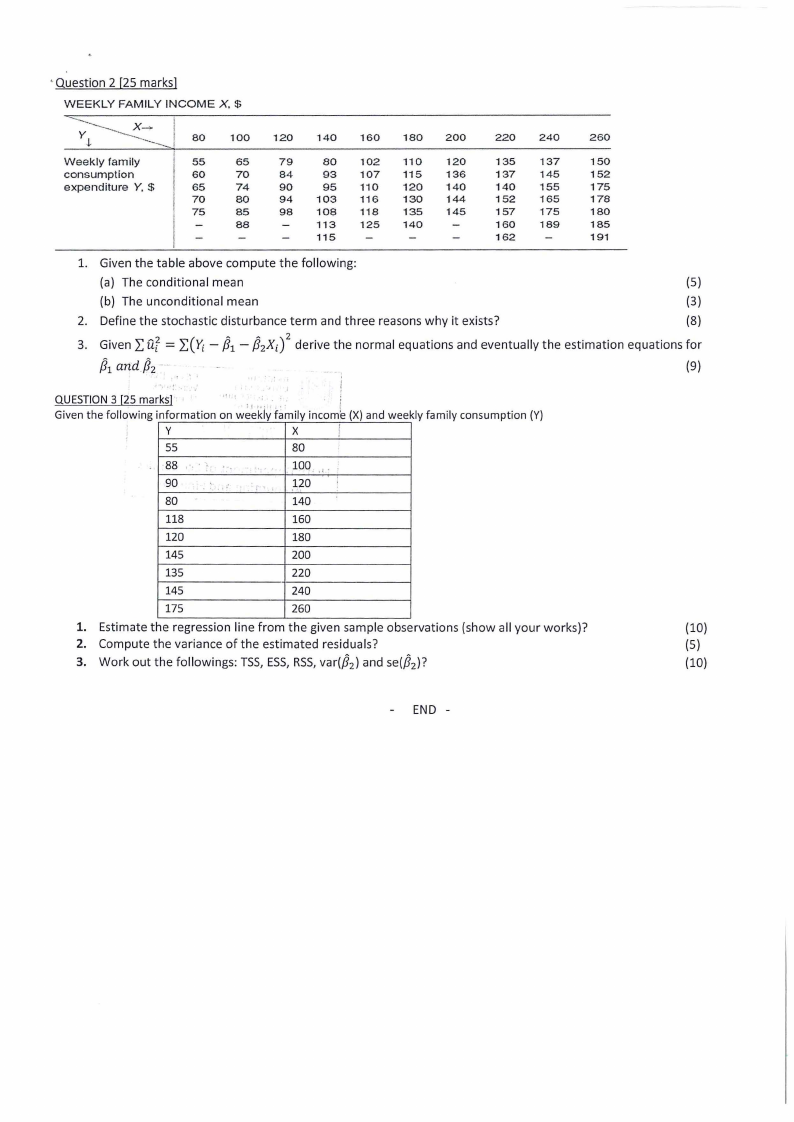

•Question 2 [25 marks]

--WEEKLY FAMILY INCOME X. $

y----- ----X- -+

80 100

120

140

160

180

200

220

240

260

.J,

---

Weekly family

55

65

79

80 102 110 120

135 137

150

consumption

60

70

84

93 107 115 136

137 145

152

expenditure Y, $

65

74

90

95 110 120 140

140 155

175

70

80

94

103

116

130

144

152

165

178

75

85

98 108 118 135 145

157 175

180

88

113 125 140

160 189

185

115

162

191

1. Given the table above compute the following:

(a) The conditional mean

(5)

(b) The unconditional mean

(3)

2. Define the stochastic disturbance term and three reasons why it exists?

(8)

= /J 3. Given 2:fl[ 2:("r-t 1 - /j2Xi)2 derive the normal equations and eventually the estimation equations for

/J1 arid /J2 ··

(9)

I

QUESTION3 [25 marks) ·

. ' . · · ·.

/

Given the following information on w~~'1dyf~mily incom 1e (X) and weekly family consumption (Y)

y

X

i

55

80

88 ,·. :

90

."

.. 100 ·' . .

r·

120 ;

80

140

118

160

120

180

145

200

135

220

145

240

175

260

1. Estimate the regression line from the given sample observations (show all your works)?

(10)

2. Compute the variance of the estimated residuals?

(5)

3. Work out the followings: TSS,ESS,RSS,var(/J2 ) and se(/J2 )?

(10)

END -