|

AMA811S-ADVANCED MANAGEMENT ACCOUNTING-1ST OPP- JUNE 2025 |

|

|

1 Page 1 |

▲back to top |

nAmlBIA unlVERSITY

OF SCIEn CE Ano TECHn

FACULTY OF COMMERCE, HUMAN SCIENCES AND EDUCATION

DEPARTMENT OF ACCOUNTING, ECONOMICS AND FINANCE

QUALIFICATION: BACHELOR OF ACCOUNTING HONOURS

QUALIFICATION

BGAC

CODE:

08 LEVEL: 8

COURSE CODE: AMA811S

COURSE NAME: ADVANCED MANAGEMENT

ACCOUNTING

DATE: MAY/JUNE 2025

DURATION: 3 HOURS

PAPER: THEORY AND CALCULATIONS

MARKS: 100

EXAMINER(S)

15T OPPORTUNITY EXAMINATION

Dr. MOSES NYAKUWANIKA

MODERATOR: LAZARUS SHINKEVA

INSTRUCTIONS

1. Capture your full name, student number and assessment number on the first

page

2. Answer ALL the questions and manage your time properly.

3. Number each page correctly

4. Write clearly and neatly.

5. Do not write in pencil and do not use tip-ex, as this will not be marked.

6. The names of people and businesses used throughout this assessment do not

reflect the reality and may be purely coincidental.

7. SHOW ALL WORKINGS!

THIS QUESTION PAPER CONSISTS OF 6 PAGES (excluding this front page)

11Page

|

|

2 Page 2 |

▲back to top |

QUESTION 1

Case study

Story is a well-established, global publishing conglomerate. The corporation is structured

to allow each country of operation to function as an autonomous business unit, that

reports back to head office. The data from each business unit is entered into the

mainframe computer at the head office. Each business unit can make use of any service

offered by other business units and can also offer services to the other units. The services

include translation into different languages, typesetting, printing, storage, and so forth. In

each country of operation, there is at least one, and usually several, retail outlets.

The core business was traditionally based upon the provision of fictional stories for the

mass market. For the past decade, Story has diversified into publishing textbooks and

technical literature. The organization currently enjoys a good reputation in both areas of

the business and global sales are increasing annually at a rate of 5% for fictional books

and 2% for textbooks. Last year seven hundred million fictional works and twenty-five

million textbooks were sold.

The corporate management team wishes to increase the growth in sales of textbooks but

realizes that they cannot afford to allocate significant resources to this task as the market,

and profit margin, for textbooks, are much smaller than for fiction. They also wish to

improve the sales performance of fictional books.

Story is currently having trouble in maintaining a corporate image in some countries of

operation. For example, several business units may be unaware of additions to the

product range. Another example is that a price change in a book is not simultaneously

altered by all the business units leading to pricing discrepancies.

Some members of the corporate management team see possible advantages to

upgrading the existing computer system to one that is fully networked. Other members

are more skeptical and are reluctant to consider enhancing the system.

YOU ARE REQUIRED TO:

(a) Discuss the issues involved in upgrading the existing information system and the

proposed changes, regarding both the wider business environment and the decision-

making process.

(18 marks}

(b) Explain what is meant by the terms open systems and closed systems as applied to

systems theory. Identify, with justification and where possible, any examples of these from

the information given in, or inferred from the case study.

(4 marks}

(c) Management Information Systems (MIS) allow managers to make timely and effective

decisions using data in an appropriate form. List three types of MIS and how they would

be used in an organization.

(3 marks}

[Total= 25 marks]

21Page

|

|

3 Page 3 |

▲back to top |

QUESTION 2

ASOP Co is considering an investment in new technology that will reduce operating costs

through increasing energy efficiency and decreasing pollution. The new technology will

cost $1 million and have a four-year life, at the end of which it will have a scrap value of

$100,000.

A licence fee of $104,000 is payable at the end of the first year. This licence fee will

increase by 4% per year in each subsequent year.

The new technology is expected to reduce operating costs by $5-80 per unit in current

price terms. This reduction in operating costs is before taking account of expected

inflation of 5% per year.

Forecast production volumes over the life of the new technology are expected to be as

follows:

Year

1

Production (units per year) 60,000

2

75,000

3

95,000

4

80,000

If ASOP Co bought the new technology, it would finance the purchase through a four-

year loan paying interest at an annual before-tax rate of 8-6% per year.

Alternatively, ASOP Co could lease the new technology. The company would pay four

annual lease rentals of $380,000 per year, payable in advance at the start of each year.

The annual lease rentals include the cost of the licence fee.

If ASOP Co buys the new technology, it can claim capital allowances on the investment

on a 25% reducing balance basis. The company pays taxation one year in arrears at an

annual rate of 30%. ASOP Co has an after tax weighted average cost of capital of 11%

per year.

YOU ARE REQUIRED TO:

(a) Based on financing cash flows only, calculate and determine whether ASOP Co

should lease or buy the new technology.

(11 marks)

(b) Using a nominal terms approach, calculate the net present value of buying the new

technology and advise whether ASOP Co should undertake the proposed

investment.

(6 marks)

(c) Discuss and illustrate how ASOP Co can use equivalent annual cost or equivalent

annual benefit to choose between new technologies with different expected lives.

(3 marks)

31Page

|

|

4 Page 4 |

▲back to top |

(d) Discuss how an optimal investment schedule can be formulated when capital is

rationed, and investment projects are either:

QUESTION 3

(i) divisible; or

(ii) non-divisible.

(5 marks)

[25 marks]

Envico is a business services company that provides seminars on various aspects of

current and recently announced changes in employment legislation. Envico has decided

to enter a one-year renewable contract with Mieras Business Associates, which owns

large premises that are suitable for holding educational seminars in each of the eight

cities.

Mieras Business Associates has offered a choice of four different contracts, each of which

relates to seminar rooms of differing sizes. These are known as room types A 8, C, and

D, which can accommodate 100, 200, 300, and 400 delegates respectively.

Envico will charge an all-inclusive fee of $80 per delegate at every seminar throughout

the year.

Envico must decide in advance of the forthcoming year which size of conference room to

contract for. It is not possible to contract for a different size conference room in different

cities, ie only one size of room can be the subject of the contract with Mieras Business

Associates.

Due to the rapid growth in interest regarding environmental issues and corporate social

responsibility, and the large amount of forthcoming legislative changes, Envico has

decided to hold one seminar every week of the year in each city. Sometimes a regional

government representative will attend and speak at such seminars. On other occasions,

a national government representative will attend and speak at such seminars. The rest of

the time the speakers at seminars are representatives from within Envico.

Envico has estimated the following frequency regarding seminars to be held during the

forthcoming year:

Category of speaker:

%

Envico representative

20

Regional government representative

50

National government representative

30

Market research has indicated that where a national government representative is in

attendance, Envico can be reasonably assured of selling 400 seminar places, and where

a regional government representative is in attendance 200 seminar places can be sold.

Envico expects to sell only 100 seminar places when there is no attendance by a

government representative.

4IPage

|

|

5 Page 5 |

▲back to top |

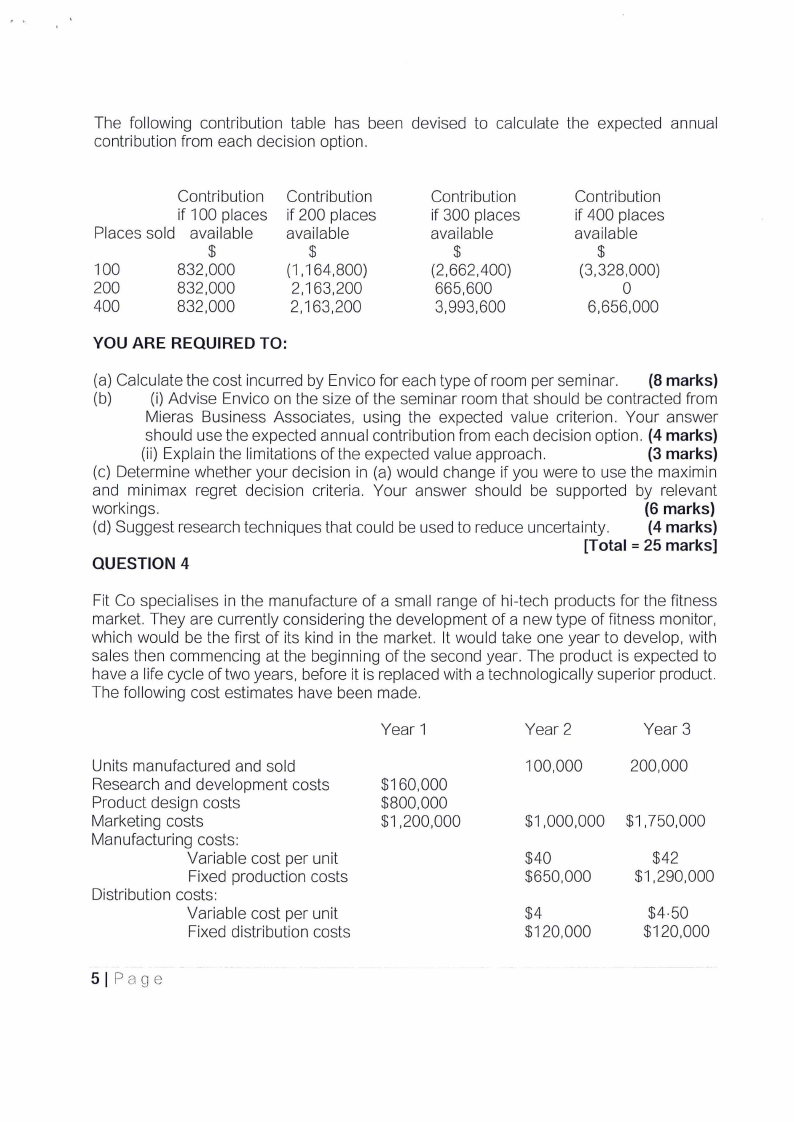

The following contribution table has been devised to calculate the expected annual

contribution from each decision option.

Contribution

if 100 places

Places sold available

$

100

832,000

200

832,000

400

832,000

Contribution

if 200 places

available

$

(1,164,800)

2,163,200

2,163,200

Contribution

if 300 places

available

$

(2,662,400)

665,600

3,993,600

Contribution

if 400 places

available

$

(3,328,000)

0

6,656,000

YOU ARE REQUIRED TO:

(a) Calculate the cost incurred by Envico for each type of room per seminar. (8 marks)

(b) (i) Advise Envico on the size of the seminar room that should be contracted from

Mieras Business Associates, using the expected value criterion. Your answer

should use the expected annual contribution from each decision option. (4 marks)

(ii) Explain the limitations of the expected value approach.

(3 marks)

(c) Determine whether your decision in (a) would change if you were to use the maximin

and minimax regret decision criteria. Your answer should be supported by relevant

workings.

(6 marks)

(d) Suggest research techniques that could be used to reduce uncertainty.

(4 marks)

[Total= 25 marks]

QUESTION 4

Fit Co specialises in the manufacture of a small range of hi-tech products for the fitness

market. They are currently considering the development of a new type of fitness monitor,

which would be the first of its kind in the market. It would take one year to develop, with

sales then commencing at the beginning of the second year. The product is expected to

have a life cycle of two years, before it is replaced with a technologically superior product.

The following cost estimates have been made.

Year1

Year2

Year3

Units manufactured and sold

Research and development costs

Product design costs

Marketing costs

Manufacturing costs:

Variable cost per unit

Fixed production costs

Distribution costs:

Variable cost per unit

Fixed distribution costs

$160,000

$800,000

$1,200,000

100,000

200,000

$1,000,000 $1,750,000

$40

$650,000

$42

$1,290,000

$4

$120,000

$4-50

$120,000

51Page

|

|

6 Page 6 |

▲back to top |

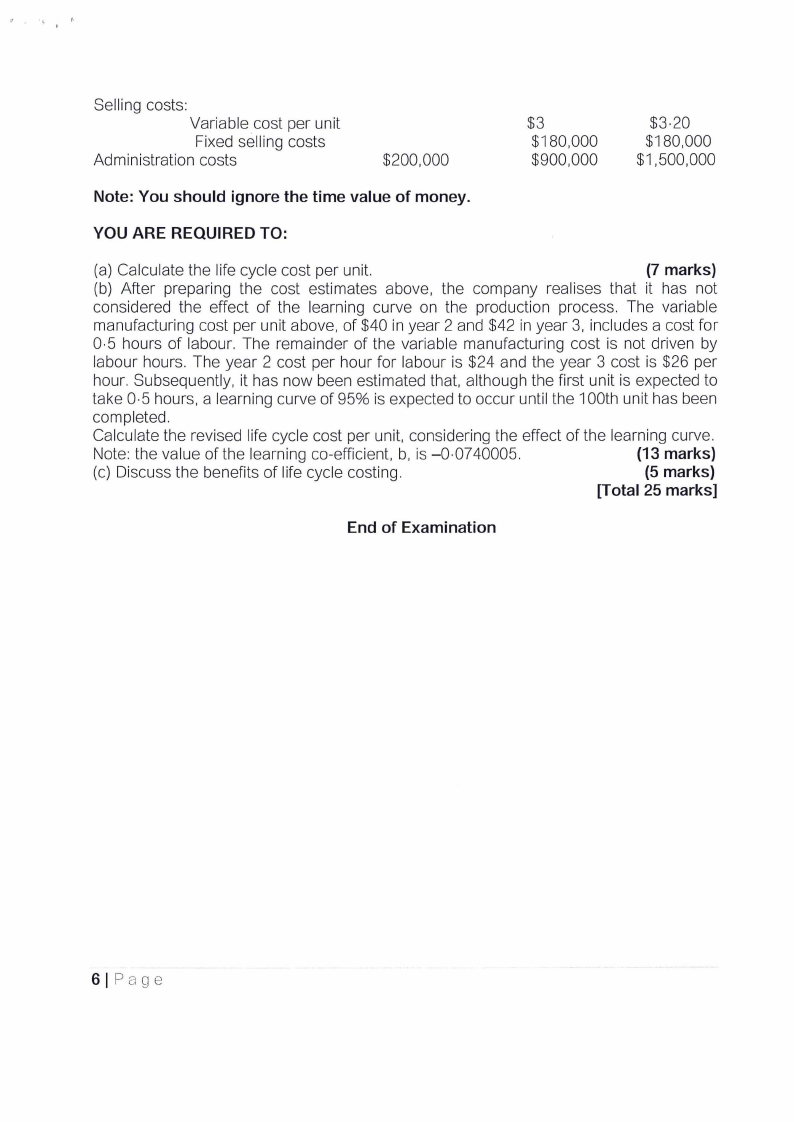

Selling costs:

Variable cost per unit

Fixed selling costs

Administration costs

$200,000

$3

$180,000

$900,000

$3-20

$180,000

$1,500,000

Note: You should ignore the time value of money.

YOU ARE REQUIRED TO:

(a) Calculate the life cycle cost per unit.

(7 marks)

(b) After preparing the cost estimates above, the company realises that it has not

considered the effect of the learning curve on the production process. The variable

manufacturing cost per unit above, of $40 in year 2 and $42 in year 3, includes a cost for

0-5 hours of labour. The remainder of the variable manufacturing cost is not driven by

labour hours. The year 2 cost per hour for labour is $24 and the year 3 cost is $26 per

hour. Subsequently, it has now been estimated that, although the first unit is expected to

take 0-5 hours, a learning curve of 95% is expected to occur until the 100th unit has been

completed.

Calculate the revised life cycle cost per unit, considering the effect of the learning curve.

Note: the value of the learning co-efficient, b, is -0-0740005.

(13 marks)

(c) Discuss the benefits of life cycle costing.

(5 marks)

[Total 25 marks]

End of Examination

61Page