|

CMA512S-COST AND MANAGEMENT ACCOUNTING 102-1ST OPP-NOV 2025 |

|

|

1 Page 1 |

▲back to top |

nAmlBIA unlVERSITY

OF SC IEn CE Ano TECH n OLOGY

FACULTY OF COMMERCE, HUMAN SCIENCES AND EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING AND FINANCE

~UALIFICATION: BACHELOR OF ACCOUNTING

QUALIFICATION CODE: 07BGAC LEVEL: 5

COURSE CODE: CMA512S

SESSION: NOVEMBER 2025

COURSE NAME: COST & MANAGEMENT ACCOUNTING 102

PAPER: THEORY AND CALCULATIONS

DURATION: 3 HOURS

MARKS: 100

FIRST OPPORTUNITY EXAMINATION QUESTION PAPER

EXAMINERS Gerhardt Sheehama , Esther Sakeus and Aina lckua

MODERATOR Helmut Namwandi

INSTRUCTIONS

1. This question paper consists of FIVE (5) questions

2. Answer ALL questions in blue or black ink only. NO PENCIL.

3. Start each question on a new page, and number the answers correctly and clearly.

4. Write clearly and neatly, showing all your formulas and workings.

5. Questions relating to this examination may be raised in the initial 30 minutes after the

start of the examination. Thereafter, candidates must use their initiative to deal with

any perceived errors or ambiguities, and any assumptions made by the candidate

should be clearly stated .

PERMISSIBLE MATERIALS

• Silent, non-programmable calculators

THIS EXAMINATION QUESTION PAPER CONSISTS OF _4_ PAGES (Excluding this cover page)

|

|

2 Page 2 |

▲back to top |

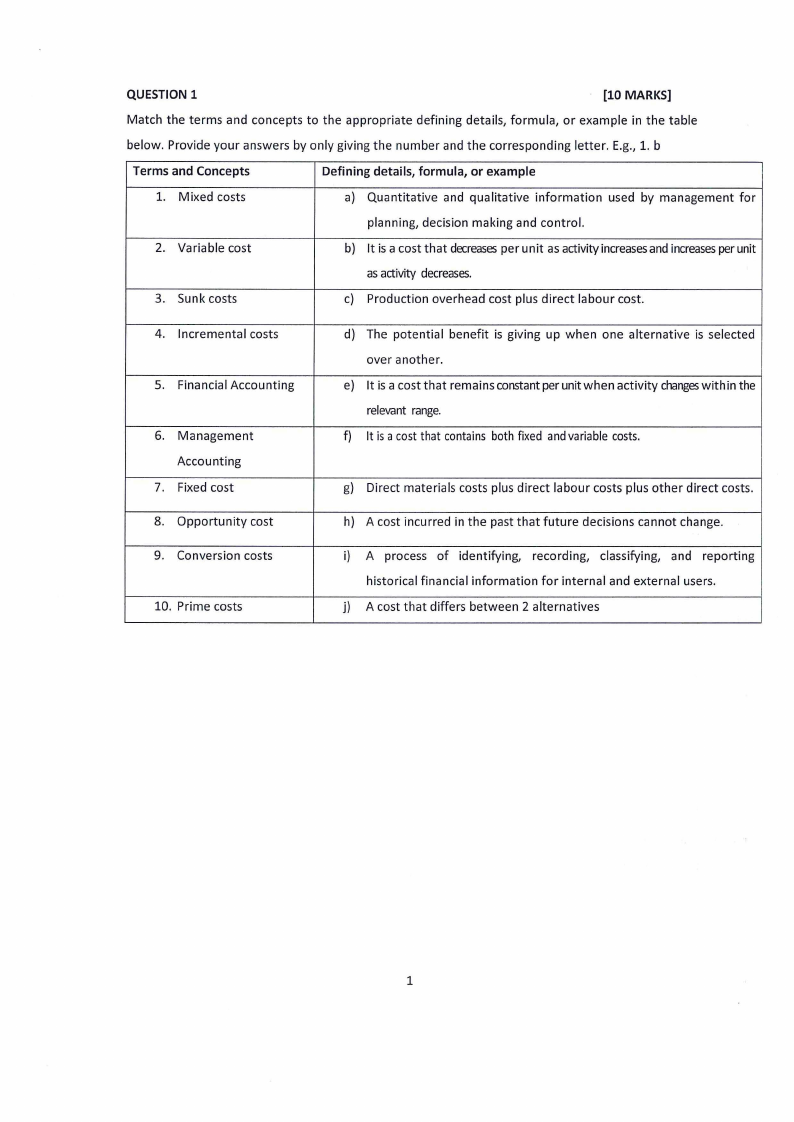

QUESTION 1

[10 MARKS]

Match the terms and concepts to the appropriate defining details, formula, or example in the table

below. Provide your answers by only giving the number and the corresponding letter. E.g., 1. b

Terms and Concepts

Defining details, formula, or example

1. Mixed costs

a) Quantitative and qualitative information used by management for

planning, decision making and control.

2. Variable cost

b) It is a cost that decreases per unit as activity increases and increases per unit

as activity decreases.

3. Sunk costs

c) Production overhead cost plus direct labour cost.

4. Incremental costs

5. Financial Accounting

6. Management

Accounting

7. Fixed cost

d) The potential benefit is giving up when one alternative is selected

over another.

e) It is a cost that remains constant per unit when activity changes within the

relevant range.

f) It is a cost that contains both fixed and variable costs.

g) Direct materials costs plus direct labour costs plus other direct costs .

8. Opportunity cost

h) A cost incurred in the past that future decisions cannot change.

9. Conversion costs

10. Prime costs

i) A process of identifying, recording, classifying, and reporting

historical financial information for internal and external users.

j) A cost that differs between 2 alternatives

1

|

|

3 Page 3 |

▲back to top |

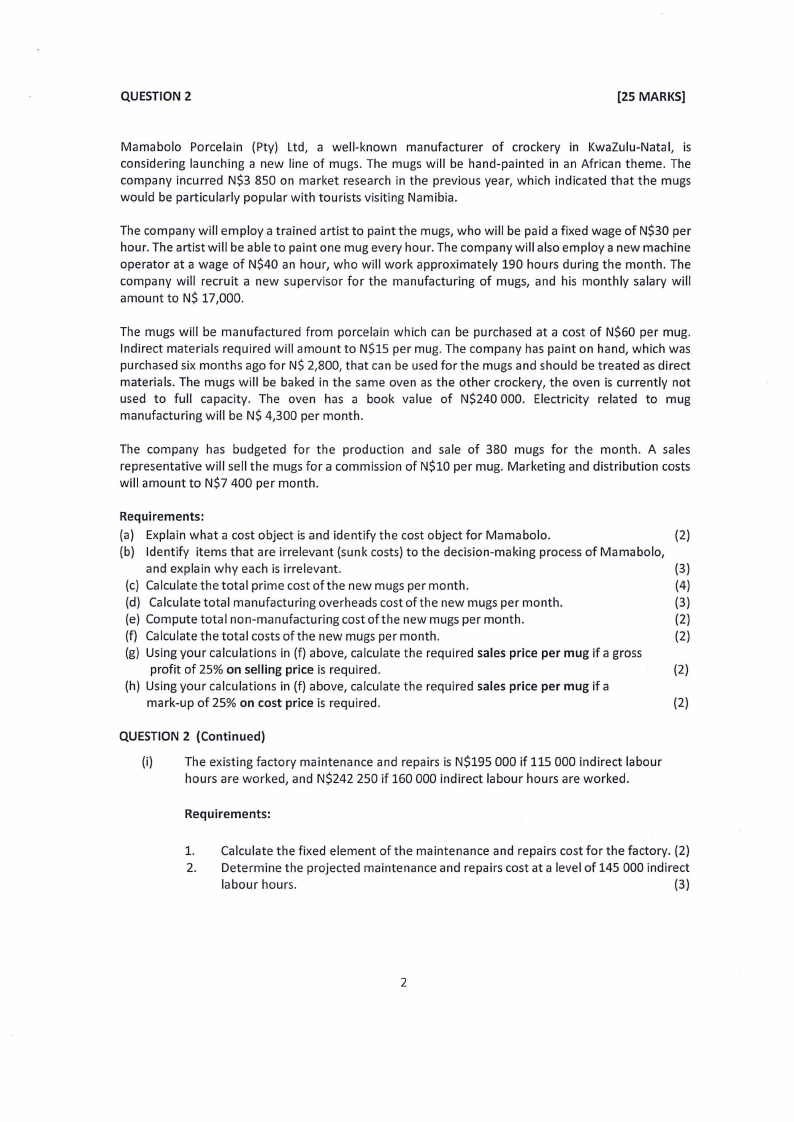

QUESTION 2

[25 MARKS]

Mamabolo Porcelain (Pty) Ltd, a well-known manufacturer of crockery in KwaZulu-Natal, is

considering launching a new line of mugs. The mugs will be hand-painted in an African theme. The

company incurred N$3 850 on market research in the previous year, which indicated that the mugs

would be particularly popular with tourists visiting Namibia.

The company will employ a trained artist to paint the mugs, who will be paid a fixed wage of N$30 per

hour. The artist will be able to paint one mug every hour. The company will also employ a new machine

operator at a wage of N$40 an hour, who will work approximately 190 hours during the month. The

company will recruit a new supervisor for the manufacturing of mugs, and his monthly salary will

amount to N$ 17,000.

The mugs will be manufactured from porcelain which can be purchased at a cost of N$60 per mug.

Indirect materials required will amount to N$15 per mug. The company has paint on hand, which was.

purchased six months ago for N$ 2,800, that can be used for the mugs and should be treated as direct

materials. The mugs will be baked in the same oven as the other crockery, the oven is currently not

used to full capacity. The oven has a book value of N$240 000. Electricity related to mug

manufacturing will be N$ 4,300 per month.

The company has budgeted for the production and sale of 380 mugs for the month. A sales

representative will sell the mugs for a commission of N$10 per mug. Marketing and distribution costs

will amount to N$7 400 per month.

Requirements:

(a) Explain what a cost object is and identify the cost object for Mama bolo.

(2)

(b) Identify items that are irrelevant (sunk costs) to the decision-making process of Mama bolo,

and explain why each is irrelevant.

(3)

(c) Calculate the total prime cost of the new mugs per month.

(4)

(d) Calculate total manufacturing overheads cost of the new mugs per month.

(3)

(e) Compute total non-manufacturing cost of the new mugs per month.

(2)

(f) Calculate the total costs of the new mugs per month.

(2)

(g) Using your calculations in (f) above, calculate the required sales price per mug if a gross

profit of 25% on selling price is required.

(2)

(h) Using your calculations in (f) above, calculate the required sales price per mug if a

mark-up of 25% on cost price is required.

(2)

QUESTION 2 (Continued)

(i)

The existing factory maintenance and repairs is N$195 000 if 115 000 indirect labour

hours are worked, and N$242 250 if 160 000 indirect labour hours are worked.

Requirements:

1. Calculate the fixed element of the maintenance and repairs cost for the factory. (2)

2. Determine the projected maintenance and repairs cost at a level of 145 000 indirect

labour hours.

(3)

2

|

|

4 Page 4 |

▲back to top |

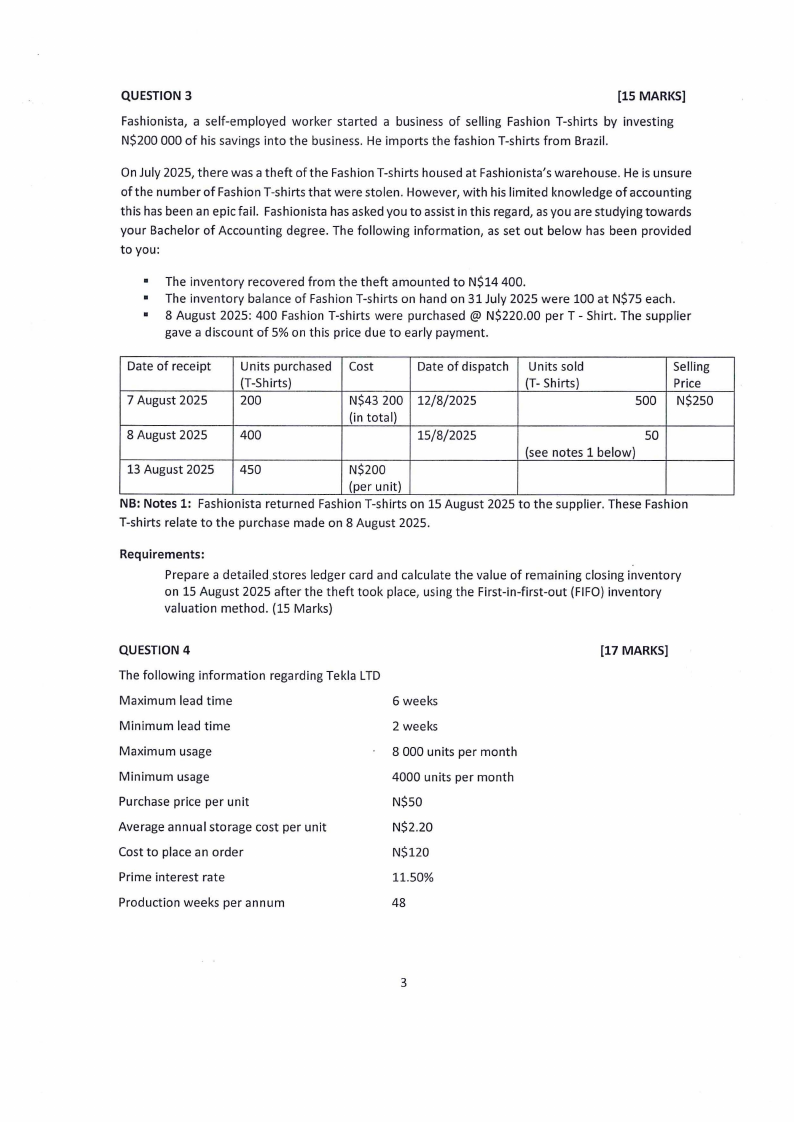

QUESTION 3

[15 MARKS]

Fashionista, a self-employed worker started a business of selling Fashion T-shirts by investing

N$200 000 of his savings into the business. He imports the fashion T-shirts from Brazil.

On July 2025, there was a theft of the Fashion T-shirts housed at Fashionista's warehouse. He is unsure

of the number of Fashion T-shirts that were stolen. However, with his limited knowledge of accounting

this has been an epic fail. Fashionista has asked you to assist in this regard, as you are studying towards

your Bachelor of Accounting degree. The following information, as set out below has been provided

to you:

• The inventory recovered from the theft amounted to N$14 400.

• The inventory balance of Fashion T-shirts on hand on 31 July 2025 were 100 at N$75 each.

• 8 August 2025: 400 Fashion T-shirts were purchased @ N$220.00 per T - Shirt. The supplier

gave a discount of 5% on this price due to early payment.

Date of receipt

Units purchased Cost

(T-Shirts)

Date of dispatch Units sold

(T- Shirts)

Selling

Price

7 August 2025

200

N$43 200 12/8/2025

500 N$250

(in total)

8 August 2025

400

15/8/2025

so

(see notes 1 below)

13 August 2025 450

N$200

(per unit)

NB: Notes 1: Fashionista returned Fashion T-shirts on 15 August 2025 to the supplier. These Fashion

T-shirts relate to the purchase made on 8 August 2025.

Requirements:

Prepare a detailed .stores ledger card and calculate the value of remaining closing inventory

on 15 August 2025 after the theft took place, using the First-in-first-out (FIFO) inventory

valuation method . (15 Marks)

QUESTION 4

The following information regarding Tekla LTD

Maximum lead time

6 weeks

Minimum lead time

2 weeks

Maximum usage

8 000 units per month

Minimum usage

4000 units per month

Purchase price per unit

N$S0

Average annual storage cost per unit

N$2.20

Cost to place an order

N$120

Prime interest rate

11.50%

Production weeks per annum

48

[17 MARKS]

3

|

|

5 Page 5 |

▲back to top |

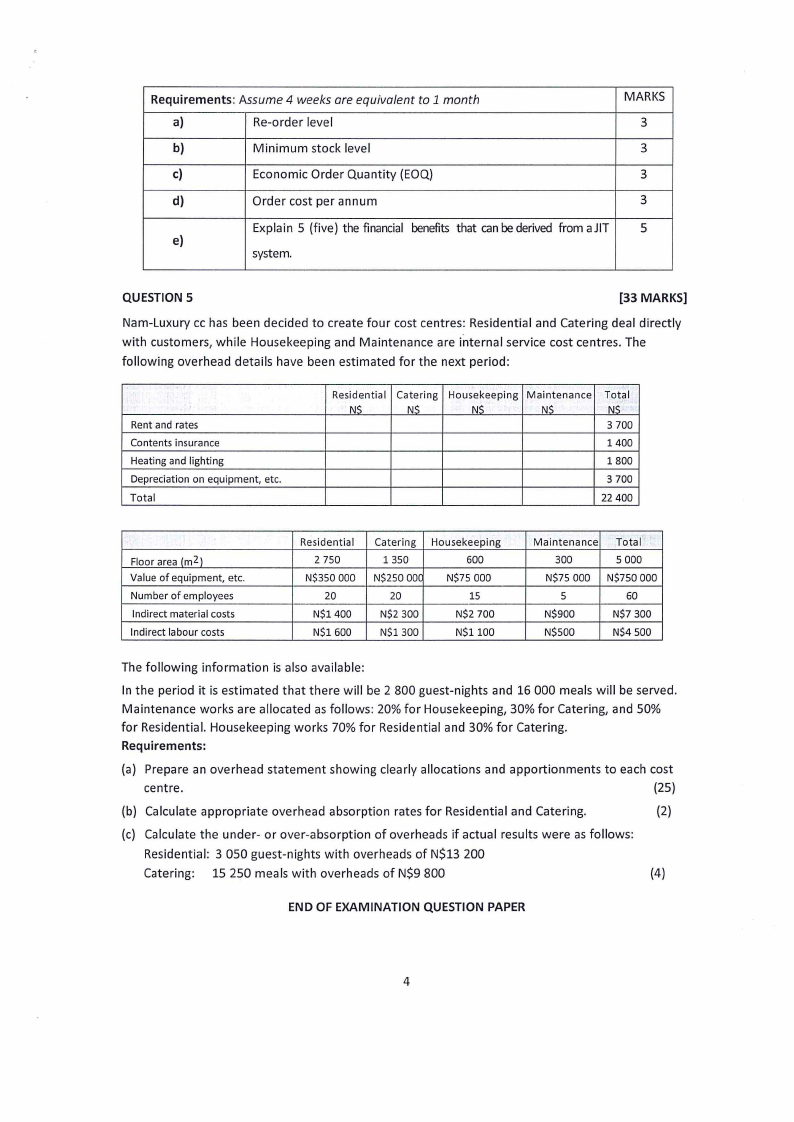

Requirements: Assume 4 weeks are equivalent to 1 month

a)

Re-order level

MARKS

3

b)

Minimum stock level

3

c)

Economic Order Quantity (EOQ)

3

d)

Order cost per annum

3

Explain 5 (five) the financial benefits that can be derived from aJIT 5

e)

system.

QUESTION 5

[33 MARKS]

Nam-Luxury cc has been decided to create four cost centres: Residential and Catering deal directly

with customers, while Housekeeping and Maintenance are internal service cost centres. The

following overhead details have been estimated for the next period:

Rent and rates

Contents insurance

Heating and lighting

Depreciation on equipment, etc.

Total

Residential

NS

Catering

NS

Housekeeping Maintenance

NS

NS

Total

NS

3 700

1400

1800

3 700

22 400

Floor area (m2 l

Value of equipment, etc.

Number of employees

Indirect material costs

Indirect labour costs

Residential

2 750

N$350 000

20

N$1400

N$1600

Catering Housekeeping

1350

600

N$250 OOC N$75 000

20

15

N$2 300

N$2 700

N$1 300

N$1100

Maintenance Total

300

5 000

N$75 000 N$750 000

5

60

N$900

N$7 300

N$500

N$4 500

The following information is also available:

In the period it is estimated that there will be 2 800 guest-nights and 16 000 meals will be served.

Maintenance works are allocated as follows: 20% for Housekeeping, 30% for Catering, and 50%

for Residential. Housekeeping works 70% for Residential and 30% for Catering.

Requirements:

(a) Prepare an overhead statement showing clearly allocations and apportionments to each cost

centre.

(25)

(b) Calculate appropriate overhead absorption rates for Residential and Catering.

(2)

(c) Calculate the under- or over-absorption of overheads if actual results were as follows:

Residential: 3 050 guest-nights with overheads of N$13 200

Catering: 15 250 meals with overheads of N$9 800

(4)

END OF EXAMINATION QUESTION PAPER

4