|

FAC512S-FINANCIAL ACCOUNTING -1ST OPP-NOV 2025 |

|

|

1 Page 1 |

▲back to top |

nAmlBIA unlVERSITY

OF SCIEnCE Ano TECHnOLOGY

FACULTY OF COMMERCE, HUMAN SCIENCES AND EDUCATION

DEPARTMENT OF ACCOUNTING, ECONOMICS AND FINANCE

QUALIFICATION: BACHELOR OF ACCOUNTING

QUALIFICATION CODE: 07BGAC

LEVEL: 5

COURSE : FINANCIAL ACCOUNTING 102

COURSE CODE: FAC512S

DATE: NOVEMBER 2025

SESSION: THEORY AND APPLICATION

DURATION: 3 HOURS

MARKS: 100

1st OPPORTUNITY EXAMINATION

FIRST EXAMINER:

Ms. H Kangala, Ms . EN Sakeus & Mr. J Angula

MODERATOR:

Mr. C Mahindi

INSTRUCTIONS

1. This question paper is made up of FIVE (5) questions.

2. Answer All the questions and in blue or black ink.

3. You are advised to pay due attention to expression and presentation. Failure to do so will

cost you marks.

4. Start each question on a new page in your answer booklet and show all your workings.

5. Questions relat ing to this paper may be raised in the initial 30 minutes after the start of

the paper. Thereafter, candidates must use their initiative to deal with any perceived error

or ambiguities and any assumption made by the candidate should be clearly stated.

PERMISSIBLE MATERIALS

Non-programmable calculator/financial calculator

THIS QUESTION PAPER CONSISTS OF 5 PAGES (Excluding this front page)

0

|

|

2 Page 2 |

▲back to top |

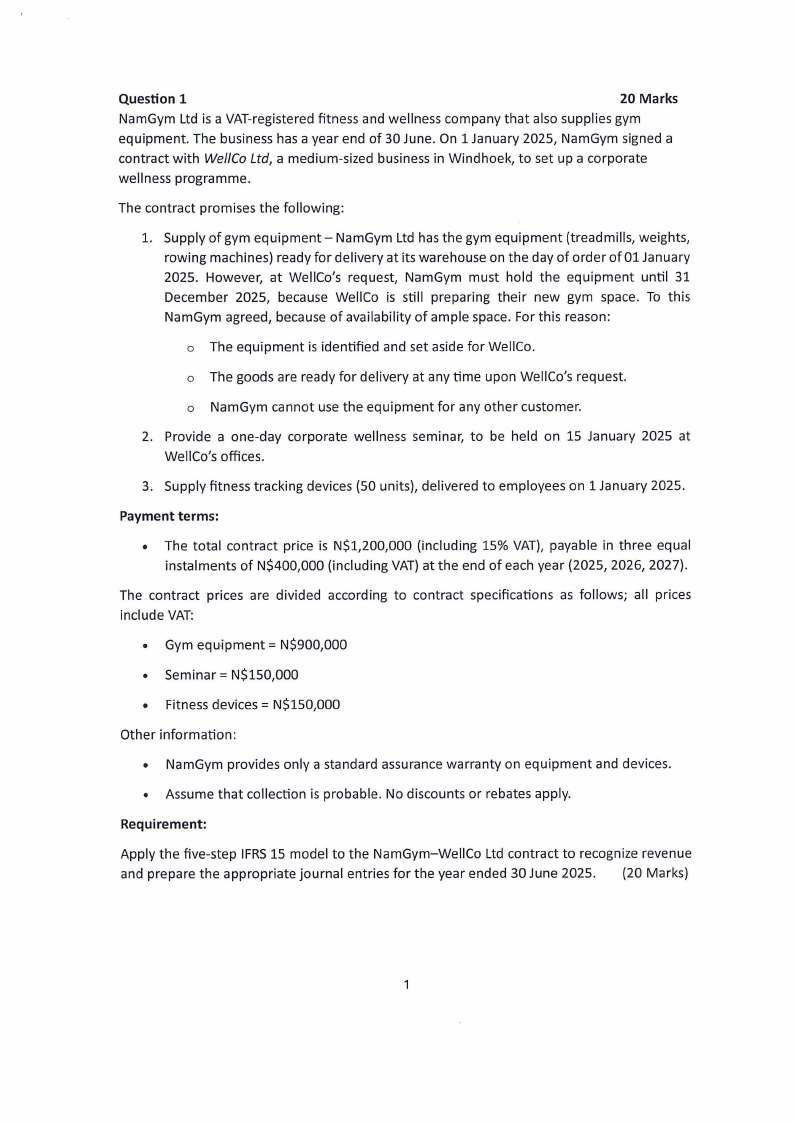

Question 1

20 Marks

NamGym Ltd is a VAT-registered fitness and wellness company that also supplies gym

equipment. The business has a year end of 30 June. On 1 January 2025, NamGym signed a

contract with Wei/Co Ltd, a medium-sized business in Windhoek, to set up a corporate

wellness programme.

The contract promises the following:

1. Supply of gym equipment- NamGym Ltd has the gym equipment (treadmills, weights,

rowing machines) ready for delivery at its warehouse on the day of order of 01 January

2025. However, at WellCo's request, NamGym must hold the equipment until 31

December 2025, because WellCo is still preparing their new gym space. To this

NamGym agreed, because of availability of ample space. For this reason:

o The equipment is identified and set aside for WellCo.

o The goods are ready for delivery at any time upon WellCo's request.

o NamGym cannot use the equipment for any other customer.

2. Provide a one-day corporate wellness seminar, to be held on 15 January 2025 at

WellCo's offices.

3. Supply fitness tracking devices (50 units), delivered to employees on 1 January 2025.

Payment terms:

• The total contract price is N$1,200,000 (including 15% VAT), payable in three equal

instalments of N$400,000 (including VAT) at the end of each year (2025, 2026, 2027).

The contract prices are divided according to contract specifications as follows; all prices

include VAT:

• Gym equ1pment = N$900,000

• Seminar= N$150,000

• Fitness devices= N$150,000

Other information:

• NamGym provides only a standard assurance warranty on equipment and devices.

• Assume that collection is probable. No discounts or rebates apply.

Requirement:

Apply the five-step IFRS 15 model to the NamGym-WellCo Ltd contract to recognize revenue

and prepare the appropriate journal entries for the year ended 30 June 2025 . (20 Marks)

|

|

3 Page 3 |

▲back to top |

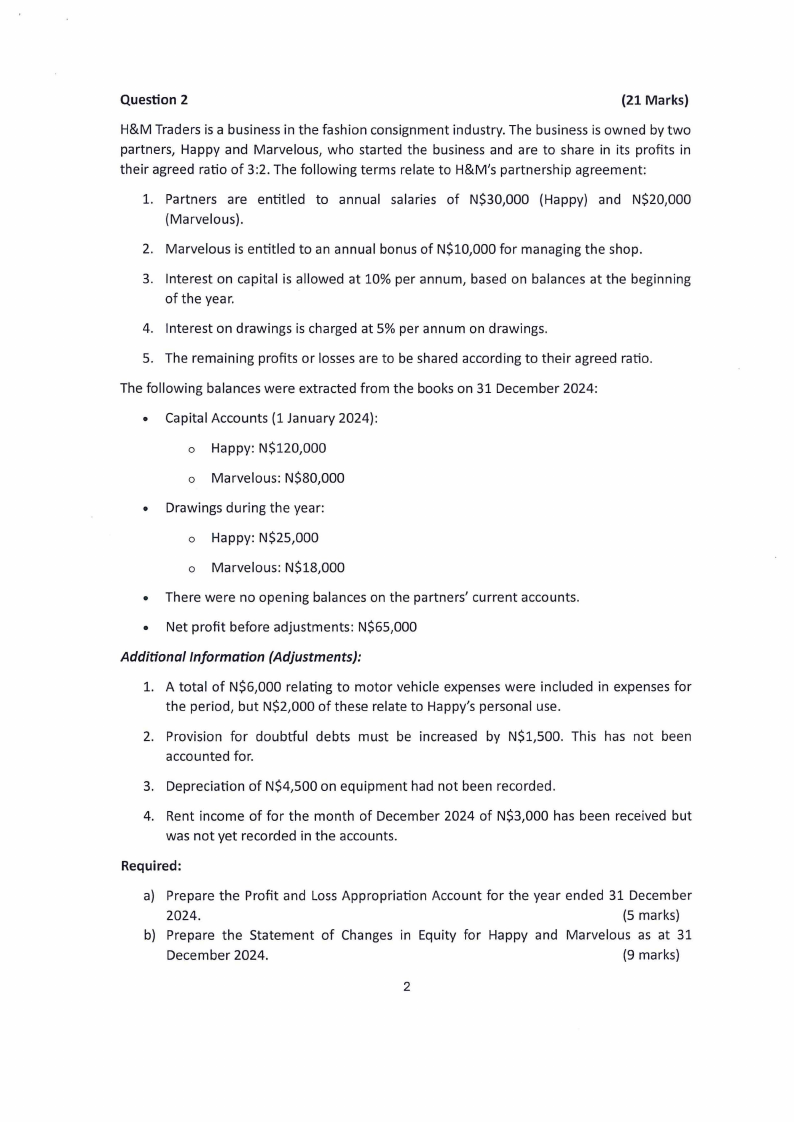

Question 2

{21 Marks)

H&M Traders is a business in the fashion consignment industry. The business is owned by two

partners, Happy and Marvelous, who started the business and are to share in its profits in

their agreed ratio of 3:2. The following terms relate to H&M's partnership agreement:

1. Partners are entitled to annual salaries of N$30,000 (Happy) and N$20,000

(Marvelous).

2. Marvelous is entitled to an annual bonus of N$10,000 for managing the shop.

3. Interest on capital is allowed at 10% per annum, based on balances at the beginning

of the year.

4. Interest on drawings is charged at 5% per annum on drawings.

5. The remaining profits or losses are to be shared according to their agreed ratio .

The following balances were extracted from the books on 31 December 2024 :

• Capital Accounts (1 January 2024) :

o Happy:N$12~000

o Marvelous: N$80,000

• Drawings during the year:

o Happy: N$25,000

o Marvelous: N$18,000

• There were no opening balances on the partners' current accounts.

• Net profit before adjustments : N$65,000

Additional Information (Adjustments):

1. A total of N$6,000 relating to motor vehicle expenses were included in expenses for

the period, but N$2,000 of these relate to Happy's persona l use.

2. Provision for doubtful debts must be increased by N$1,500. This has not been

accounted for.

3. Depreciation of N$4,500 on equ ipment had not been recorded .

4. Rent income of for the month of December 2024 of N$3,000 has been received but

was not yet recorded in the accounts.

Required:

a) Prepare the Profit and Loss Appropriation Account for the year ended 31 December

2024.

(5 marks)

b) Prepare the Statement of Changes in Equity for Happy and Marvelous as at 31

December 2024.

(9 marks)

2

|

|

4 Page 4 |

▲back to top |

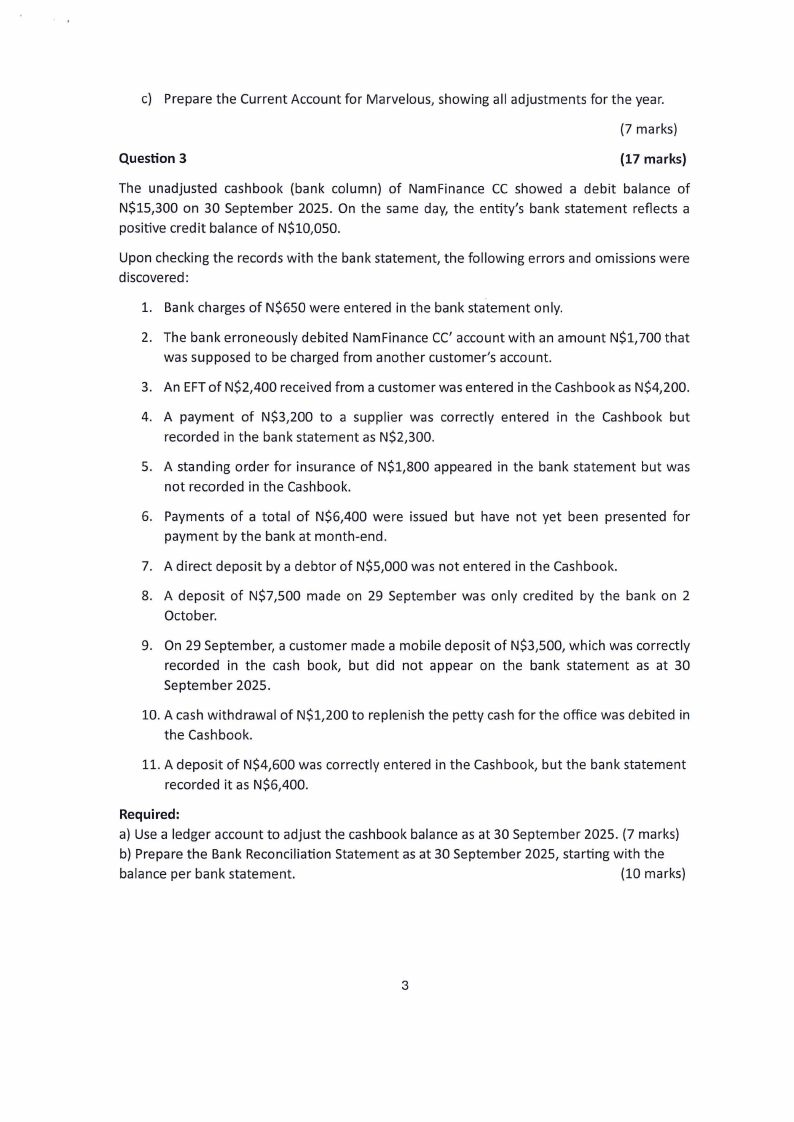

c} Prepare the Current Account for Marvelous, showing all adjustments for the year.

(7 marks}

Question 3

{17 marks)

The unadjusted cashbook (bank column) of NamFinance CC showed a debit balance of

N$15,300 on 30 September 2025 . On the same day, the entity's bank statement reflects a

positive credit balance of N$10,050.

Upon checking the records with the bank statement, the following errors and omissions were

discovered :

1. Bank charges of N$650 were entered in the bank statement only.

2. The bank erroneously debited Nam Finance CC' account with an amount N$1, 700 that

was supposed to be charged from another customer's account.

3. An EFT of N$2,400 received from a customer was entered in the Cashbook as N$4,200.

4. A payment of N$3,200 to a supplier was correctly entered in the Cashbook but

recorded in the bank statement as N$2,300.

5. A standing order for insurance of N$1,800 appeared in the bank statement but was

not recorded in the Cashbook.

6. Payments of a total of N$6,400 were issued but have not yet been presented for

payment by the bank at month-end .

7. A direct deposit by a debtor of N$5,000 was not entered in the Cashbook.

8. A deposit of N$7,500 made on 29 September was only credited by the bank on 2

October.

9. On 29 September, a customer made a mobile deposit of N$3,500, which was correctly

recorded in the cash book, but did not appear on the bank statement as at 30

September 2025.

10. A cash withdrawal of N$1,200 to replenish the petty cash for the office was debited in

the Cashbook.

11. A deposit of N$4,600 was correctly entered in the Cashbook, but the bank statement

recorded it as N$6,400.

Required:

a} Use a ledger account to adjust the cashbook balance as at 30 September 2025. (7 marks}

b} Prepare the Bank Reconciliation Statement as at 30 September 2025, starting with the

balance per bank statement.

(10 marks}

3

|

|

5 Page 5 |

▲back to top |

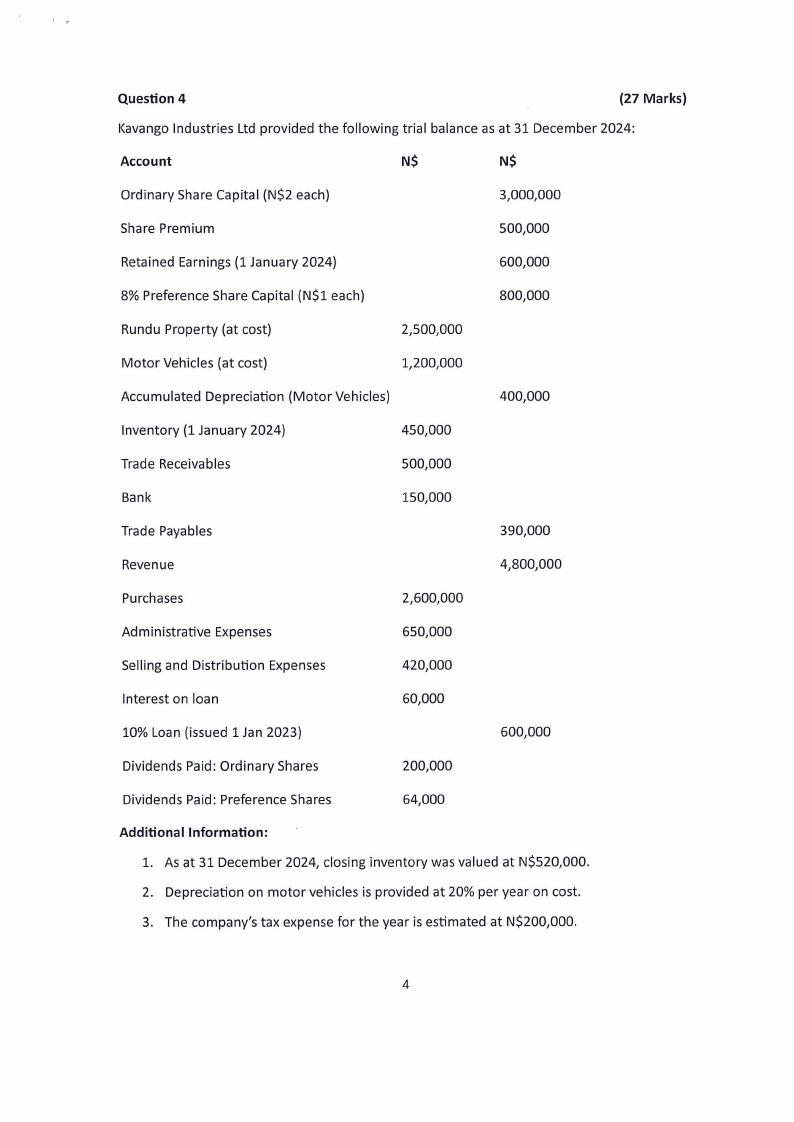

Question 4

(27 Marks)

Kavango Industries Ltd provided the following trial balance as at 31 December 2024:

Account

N$

N$

Ordinary Share Capital (N$2 each)

3,000,000

Share Premium

500,000

Retained Earnings (1 January 2024)

600,000

8% Preference Share Capital (N$1 each)

800,000

Rundu Property (at cost)

2,500,000

Motor Vehicles (at cost)

1,200,000

Accumulated Depreciation (Motor Vehicles)

400,000

Inventory (1 January 2024)

450,000

Trade Receivables

500,000

Bank

150,000

Trade Payables

390,000

Revenue

4,800,000

Purchases

2,600,000

Administrative Expenses

650,000

Selling and Distribution Expenses

420,000

Interest on loan

60,000

10% Loan (issued 1 Jan 2023}

600,000

Dividends Paid: Ordinary Shares

200,000

Dividends Paid: Preference Shares

64,000

Additional Information:

1. As at 31 December 2024, closing inventory was valued at N$520,000.

2. Depreciation on motor vehicles is provided at 20% per year on cost.

3. The company's tax expense for the year is estimated at N$200,000.

4

|

|

6 Page 6 |

▲back to top |

4. The company has 1,500,000 of issued ordinary shares, with no new shares issued

during the year.

5. The directors propose a final dividend of N$0.10 per ordinary share on 15 December

2024.

6. The Rundu Property was revalued upwards by N$300,000 during the year to its current

value of N$2,500,000.

Required:

a) Prepare the Statement of Profit or Loss and Other Comprehensive Income for Kavango

Industries Ltd for the year ended 31 December 2024 in accordance to the presentation

requirements of IFRS 18.

(12 marks)

b) Prepare the Statement of Changes in Equity for the year ended 31 December 2024.

(10 marks)

c) Calculate the Earnings per Share (EPS) for the year ended 31 December 2024. (5 marks)

Question 5

15 Marks

Sunrise Fitness Club received N$60,000 on 1 October 2024 for annual membership

subscriptions. The amount covers the period 1 October 2024 to 30 September 2025. The

accountant of the club recorded the entire N$60,000 as income for the year ended 31

December 2024.

However, during the audit, the auditor questioned whether the full amount should be treated

as income or partly as a liability.

Required:

Using the definitions of income and liabilities from the Conceptual Framework, discuss

whether the subscription received should be treated fully as income, or partly as income and

partly as a liability. Give specific amounts and justify your answer.

(5 marks)

4.2. Answer the following questions:

i.

Explain the qualitative characteristic of relevance.

(2 Marks)

ii.

Explain the objective of general purpose of financial statements.

(2 Marks)

iii. Explain the accrual basis concept.

(2 Marks)

iv. Explain the meaning of profitability ratios in financial analysis.

v.

Discuss one limitation of ratio analysis.

(2 marks)

(2 marks)

End of Question paper

5